Are euro area inflation expectations de-anchoring from the ECB target?

Tight anchoring of long-term inflation expectations around the central bank's inflation target is a precondition for price stability. It prevents undesirable short-term inflation fluctuations from passing through to the wage and price formation. In this article, we use micro-data from the ECB Survey of Professional Forecasters to examine whether inflation expectations have changed significantly during recent years and whether they are still anchored to the ECB's inflation target.

The ECB Survey of Professional Forecasters (SPF) is the longest-running survey of its kind in Europe. Since 1999, the ECB has been conducting a quarterly survey of dozens of economists on their inflation expectations in the euro area. Typically, five-year inflation expectations are an indicator used by monetary policy makers and scholars to determine whether inflation expectations are anchored to the ECB's medium-term objective of "below but close to 2%".

Why is it important for us to analyse what a few dozens of economists think about inflation developments in the future? (especially because they have not done too well with their long-term forecasting: the correlation between their five-year inflation expectations and the actual inflation recorded five years later is close to zero). Nevertheless, such analysis is important because labour market participants set wages and entrepreneurs set product prices according to their current expectations of future inflation. The economy works best when market participants are confident in price stability, i.e. low and predictable inflation. When prices are expected to fall, a deflationary spiral might be triggered as consumers postpone their purchases while companies lay off workers and lower wages, thus further reducing demand for goods and services. Conversely, when prices are expected to rise unsustainably, confidence decreases and interest rates on loans rise, thereby discouraging investment. Economy suffers in both cases.

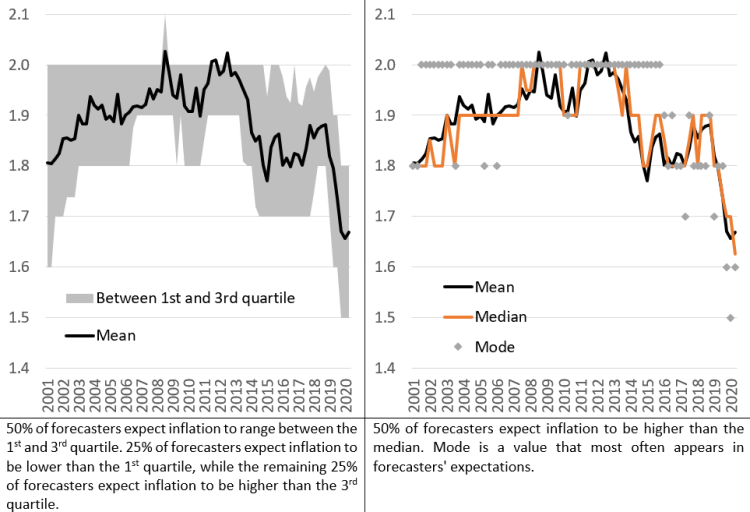

1. Euro area five-year inflation expectations slipped below 2%

At first glance, it seems that euro area five-year inflation expectations of professional forecasters are firmly anchored to the ECB target "below but close to 2%". Over the last 20 years, the average point forecast for inflation in five years' time has never been below 1.65% or higher than 2.05% (see Figure 1).

However, it is also true that five-year inflation expectations in the euro area have never been as low as today. Until 2016, professional forecasters commonly thought that inflation in five years would be 2.0%. Currently, however, they are much more likely to forecast 1.5% or 1.6%. More specifically, a few years ago three out of four professional forecasters thought that inflation in five years would be no less than 1.9%. Today, three out of four forecasters expect it to be no higher than 1.8%.

Figure 1. Euro area five-year inflation expectations: point forecast

2. Euro area five-year inflation expectations are increasingly subject to downside risks

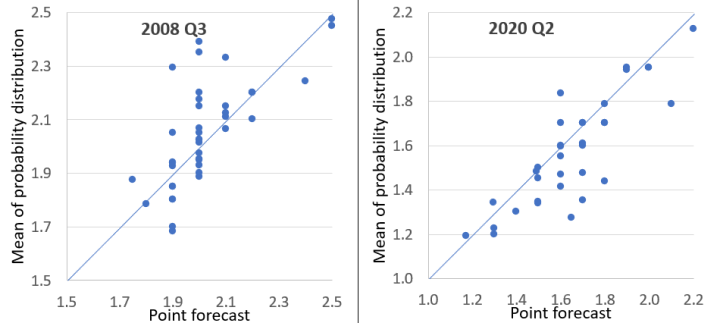

In addition to the point forecasts (e.g. 1.7%), economists also indicate their probability distribution (for example, there is a 60% probability that inflation will be in the range between 1.5-1.9%; and a 40% probability that it will be in the range between 2.0-2.4%). The difference between the mean value of the probability distribution and the point forecast reflects the balance of risks, an indicator reflecting professional forecasters' view on the downside or upside risks to inflation.

Last year's five-year inflation expectations based on the probability distribution are lower than the point forecast. This suggests downside risks to inflation expectations. For example, in the second quarter of 2020, the mean probability distribution values of most economists' inflation expectations were significantly lower than their respective point forecasts. By comparison, most economists pointed to upside risks in 2008 when euro area inflation temporarily rose to almost 4% due to a surge in oil prices (see Figure 2).

Figure 2. Euro area five-year inflation expectations: mean point forecast and mean of probability distribution

Notes. The dots indicate the euro area five-year inflation expectations of individual forecasters. In the third quarter of 2008, forecasters reported their inflation projections for 2013. In the second quarter of 2020, forecasters posted their inflation projections for 2024.

Of course, risks to inflation expectations do not always materialise. For example, in 2008 forecasters pointed to upside risks; however, in 2013, i.e. five years later, inflation turned out to be lower than expected. The balance of risks could indicate whether inflation expectations are more sensitive to positive or negative economic shocks. The fact that the balance of risks has been systematically negative for several years suggests that a decline in inflation might have a greater impact on long-term expectations than a rise in inflation (see Section 4).

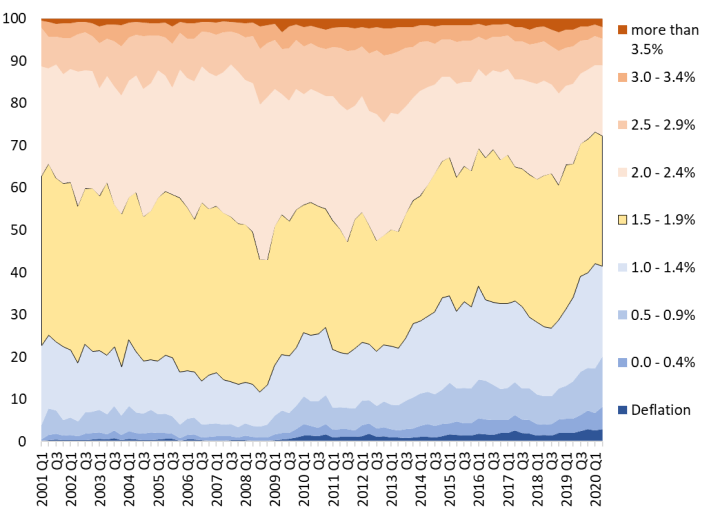

Five-year inflation expectations deteriorated against the backdrop of an increasing probability of low inflation and a decreasing probability of high inflation. The probability that inflation will exceed 2% in five years has fallen to about one quarter, whereas the probability of low inflation, i.e. 1.4% and below, has increased significantly (see Figure 3).

Figure 3. Probability distribution of euro area five-year inflation expectations

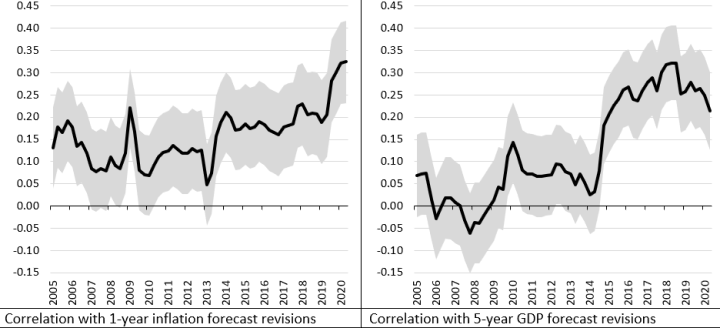

3. Five-year inflation expectations have become more responsive to macroeconomic variables

The SPF survey is designed as a rotating panel with many forecasters providing their projections during several consecutive quarters. This allows us to analyse the changes in the five-year inflation expectations of individual forecasters over time and their relationship to changes in the projections of other macroeconomic variables.

Our estimates show that five-year inflation expectations are often adjusted along with other macroeconomic variables. For instance, forecasters who adjust their five-year inflation expectations also adjust inflation expectations for the next year as well as their projections of economic growth in five years (see Figure 4). An increase in correlation over time is another evidence that five-year inflation expectations are less firmly anchored to the ECB's inflation target. Moreover, a higher correlation with long-term GDP projections since 2015 could point to secular stagnation risks.

Figure 4. Changes in euro area five-year inflation expectations: correlation with changes in short-term inflation projections and GDP projections

Notes. Expectations are defined here as the mean of probability distributions reported by professional forecasters. The black line indicates the 16-quarter rolling correlation, the grey area is the 95% confidence interval of the correlation coefficient. Dates indicate the end of the 16-quarter window.

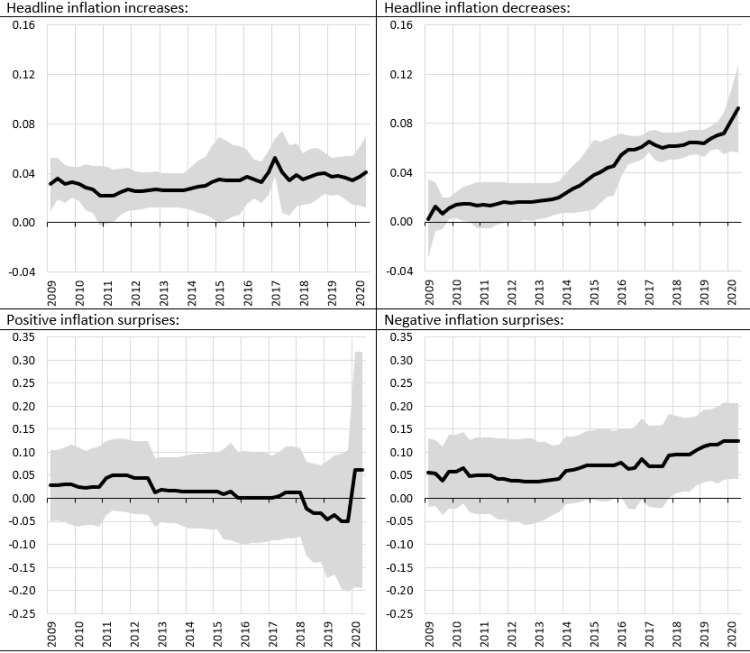

4. Sensitivity of five-year inflation expectations is asymmetric

The sensitivity of five-year inflation expectations to actual inflation and inflation forecast errors is asymmetric. Our results suggest that, over the past few years, five-year inflation expectations have tended to react more to a decrease rather than an increase in inflation (see Figure 5). Namely, the negative balance of risks (see Section 2) is reflected in the fact that inflation expectations are particularly sensitive to falling inflation.

Next, we analyse whether five-year inflation expectations respond to the fact that inflation has been under- or overprojected. Our results show that five-year inflation expectations hardly respond to positive inflation surprises, i.e. underprojected inflation: the elasticity is close to zero. Meanwhile, in recent years inflation expectations have responded significantly to negative inflation surprises, i.e. overprojected inflation. In other words, if actual inflation turns out to be lower than projected, economists tend to adjust their five-year inflation expectations downwards.

Figure 5. Sensitivity of euro area five-year inflation expectations to headline inflation developments and headline inflation surprises

Notes: The black line indicates elasticity over the rolling window of 29-quarters, the grey area is the 95% confidence interval of this elasticity. Dates indicate the end of the 29-quarter window. Inflation surprises are obtained as the difference between the Eurostat flash inflation estimate and the economists' median forecast surveyed by Bloomberg shortly before the publication of the Eurostat flash. We use the cumulative forecast error between two consecutive SPF surveys.

Conclusion

Euro area inflation expectations remain anchored to the ECB's inflation target. Five-year inflation expectations are significantly more stable and closer to 2% compared to headline inflation and short-term inflation expectations. Five-year inflation expectations are also much less responsive to actual inflation than one- or two-year inflation expectations. However, it is also clear that the link between five-year inflation expectations and the ECB's medium-term inflation target has weakened. Hence, the introduction of new ECB instruments in case of adverse economic shocks is justified.

We showed in this article that five-year inflation expectations are (i) heading downwards, (ii) sensitive to changes in macroeconomic variables, (iii) sensitive to falling inflation and negative inflation surprises. Do these findings have macroeconomic implications?

In recent years, wage growth in the euro area has not been in line with fundamental factors and unemployment dynamics. It was also lower than economists had predicted. Such developments could have underpinned a decline in inflation expectations as from 2013. Slow wage growth in 2019 may further exert downward pressure on longer-term inflation expectations. A series of downward spiral effects between inflation expectations and wages may signal increasing risks of disinflation, especially in view of the fact that a negative risk balance and a particular sensitivity of inflation expectations to the negative shocks create room for further downward steps. True, with five-year inflation expectations hovering around 1.6%, the probability of prolonged deflation is still low. Nonetheless, the impact of a potential disinflationary spiral on the economy is so extremely negative that every effort must be made to rule it out completely.

Literature

Corsello F., Neri S., Tagliabracci A (2019). Anchored or de-anchored? That is the question. Bank of Italy Occasional Paper nr.516.

Dovern, J., Kenny, G. (2020). Anchoring Inflation Expectations in Unconventional Times: Micro Evidence for the Euro Area. International Journal of Central Banking, forthcoming.

Łyziak T., Paloviita M. (2017). Anchoring of inflation expectations in the euro area: recent evidence based on survey data. European Journal of Political Economy, vol. 46(C), pp. 52-73.

Textual error

«… …»