Latvia's Macro Profile. June 2023

Latvijas Banka has published its latest June 2023 macroeconomic forecasts drawn up amid persistently high uncertainty.

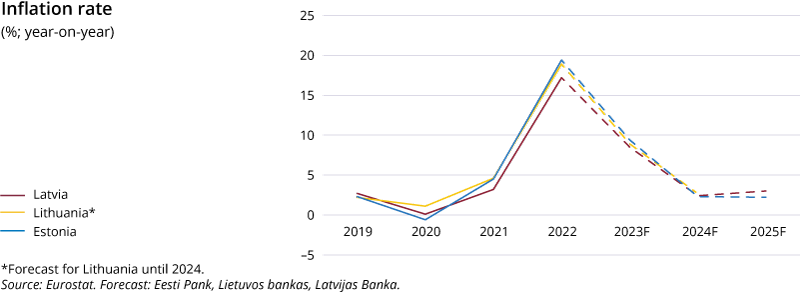

- Latvia's inflation projections for 2023 and 2024 have been revised downwards to 8.5% and 2.4% respectively (the March 2023 projections were 10.0% and 2.7% respectively). For 2025, inflation has been revised slightly upwards – to 3.0% (the March projection – 2.6%).

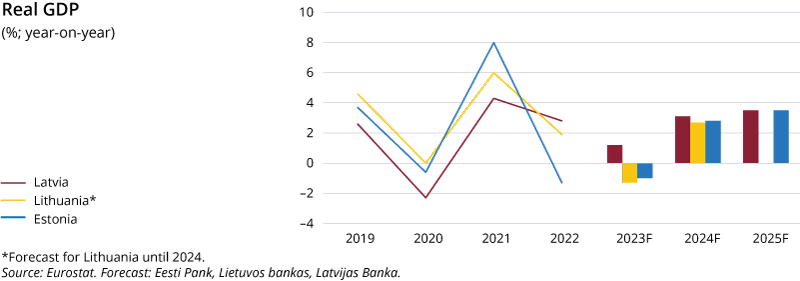

- The gross domestic product (GDP) growth forecast for 2023 has been revised upwards to 1.2% (the March forecast – 0.5%) therefore GDP growth, compared to the March forecast, is revised downwards to 3.1% in 2024 (the March forecast was 3.7%). GDP growth forecast for 2025 is 3.5% (the March forecast stood at 3.3%).

- Inflation in the euro area is proving to be more persistent than previously expected despite falling energy prices and easing supply chain bottlenecks.

- With global energy and food prices decreasing, it is expected that headline inflation in the euro area will continue on a downward path; however, core inflation (excluding food and energy prices) will be more persistent in combination with increasing labour costs and stronger demand in the services sector.

- In the light of inflation outlook continuing to be too high for too long, the Governing Council of the European Central Bank (ECB) has decided to continue raising interest rates by 25 basis points in May and June respectively.

- The ECB's future decisions will ensure that the key ECB interest rates will be brought to levels sufficiently restrictive to achieve a timely return of inflation to the 2% medium-term target and will be kept at those levels for as long as necessary.

- Annual inflation in Latvia continues decreasing on a monthly basis, i.e. from inflation rates exceeding 20% early this year to 12.3% in May, and it is expected that inflation in Latvia will decline to single digit levels in the second half of 2023.

- Electricity prices and the administratively regulated heat energy and water supply tariffs also decrease in Latvia along with a drop in global energy prices. Lower natural gas tariffs for households also reflect growing competition in Latvia's natural gas market. Higher tariffs of electricity transmission and distribution services will take effect as of July, but they leave the outlook for inflation unchanged, since they were already included in the previous forecasts as pending ones.

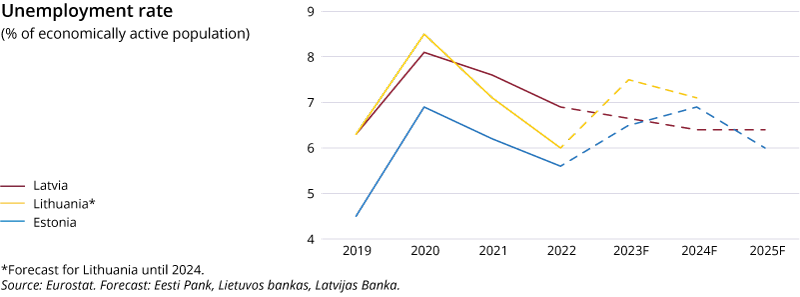

- The low unemployment entails an advantage for employees to request wage growth to maintain their purchasing power.

- A lower energy cost burden enables businesses to increase remuneration of sought-after employees.

- Wages already edged up by 12% in the first quarter, reflecting a rise in the minimum wage and partly compensating the impact of inflation.

- The previous changes in wages, which occurred amid the high inflation experienced earlier, in combination with the support available to households in the next heating season will maintain the purchasing power of households.

- However, the second-round inflation risks intensify: if employees request higher wages to compensate for inflation on the basis of high inflation expectations and businesses offset the sharply increasing labour costs by price rises, inflation may remain higher than the desired rates for an extended period of time.

- Such a wage-price spiral, which is not the baseline scenario of Latvijas Banka's forecasts, would significantly harm competitiveness and the economy as a whole.

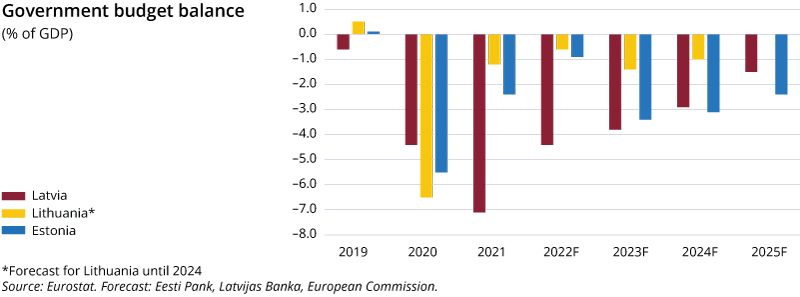

- Currently, inflation expectations are decreasing, and the government support is intended to be more targeted to avoid fuelling inflation, which is an important aspect. As lower government support expenditure and higher economic activity are envisaged, the general government deficit will gradually fall from 3.8% of GDP in 2023 over the coming years.

- The wage growth incorporated in the forecast baseline scenario justifies an upward revision of the core inflation forecast for this year to 8.2% (the March forecast – 7.7%), and it will remain above 4% over the medium term due to the tight labour market.

- The surprisingly vigorous private consumption seen at the end of 2022 and better growth observed early this year, primarily due to growing investments, change the outlook of developments taking place this year.

- An earlier than projected depletion of savings for purchases , will limit consumption growth in the coming quarters. Faster upswing in consumption will begin only in 2024 when inflation rates moderate, and Latvia's economic growth will also accelerate in 2024–2025.

- At present, costs of energy and other resources are normalising; however, uncertainty prevailing in the region and the rising borrowing costs will weigh on investment growth. The role of European Union funds is increasing amid uncertainty; however, the implementation of projects has experienced delays so far.

- Demand forecasts in the main trade partners, particularly in Estonia and Lithuania, also hamper Latvia's economic growth.

Macroeconomic fundamentals: Latvijas Banka's June 2023 forecasts

|

2023 |

2024 |

2025 |

|

|

Economic activity (annual changes; %; at constant prices; seasonally adjusted data) |

|

||

|

GDP |

1.2 |

3.1 |

3.5 |

|

Private consumption |

1.3 |

3.9 |

4.4 |

|

Government consumption |

–4.4 |

–0.1 |

0.5 |

|

Investment |

0.4 |

4.9 |

6.1 |

|

Exports |

–0.1 |

3.0 |

3.1 |

|

Imports |

–42.5 |

2.8 |

3.6 |

|

HICP inflation (annual changes; %) |

|

||

|

Inflation |

8.5 |

2.4 |

3.0 |

|

Core inflation (excluding food and energy prices) |

8.2 |

5.7 |

4.4 |

|

Labour market |

|

||

|

Unemployment (% of the economically active population; seasonally adjusted data) |

6.7 |

6.4 |

6.4 |

|

Nominal gross wage (annual changes; %) |

12.0 |

8.2 |

7.8 |

|

External sector |

|

||

|

Current account balance (% of GDP) |

–3.4 |

–3.6 |

–4.3 |

|

Government finances (% of GDP) |

|

||

|

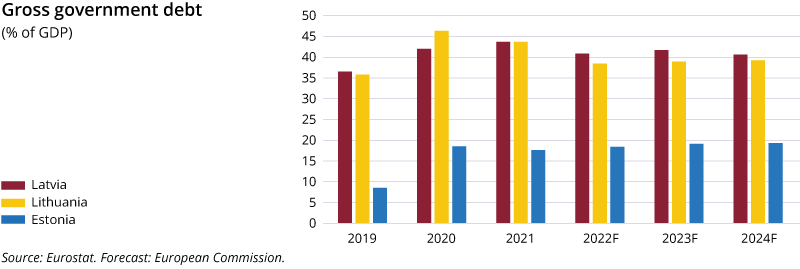

General government debt |

41.7 |

40.6 |

40.1 |

|

Budget surplus/deficit |

–3.8 |

–2.9 |

–1.5 |

The forecasts were finalised on 31 May 2023. The cut-off date for some technical assumptions was the 23 May.

Textual error

«… …»