Latvia's Macro Profile. December 2023

Latvijas Banka has revised its macroeconomic forecasts

Latvijas Banka has published its latest December 2023 macroeconomic forecasts. Inflation in Latvia is expected to be low (2.0%) in 2024; however, the growth of gross domestic product (GDP) will remain weak (2.0%). The latest forecasts have been drawn up amid persistently high uncertainty.

The restrictive monetary policy significantly reduces inflation in the euro area and Latvia.

According to the latest Eurosystem staff projections for the euro area, inflation is expected to decline gradually over the course of next year, before approaching the Governing Council's 2% target in 2025.

The Governing Council considers that the key ECB interest rates (including the deposit facility rate of 4.0%) are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal.

The ECB's future interest rate decisions will be based on its assessment of the inflation outlook, including in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission.

The Governing Council decided to advance the normalisation of the Eurosystem's balance sheet, intending to reduce the pandemic emergency purchase programme (PEPP) portfolio by 7.5 billion euro per month on average over the second half of the year.

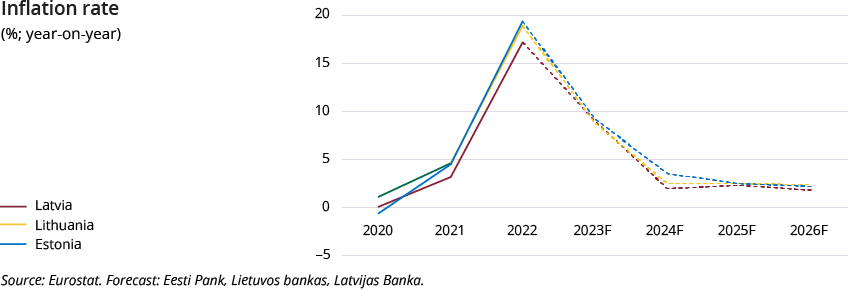

Inflation in Latvia has returned to a low level and is lower than the EU average.

Prices have decreased in the last months of this year mainly due to the sharp fall in global energy prices. In Latvia, this is reflected in lower heat energy and fuel prices, which also reduce the pressure on the prices of other goods and services.

Annual inflation is declining every month from the very high levels observed in the first half of the year to stand at 1.1% in November. The inflation estimate for 2023 stands at 9.0%, which corresponds to Latvijas Banka's September forecasts.

Inflation is projected to stand at around 2% over the next three years (2.0%, 2.3% and 1.8% in 2024–2026 respectively). The government's decisions on raising indirect tax rates and on limiting the increase in electricity distribution tariffs are among the factors affecting inflation. However, the assumptions about lower than previously estimated global prices of natural gas, oil and food have affected both the downward revision of inflation forecasts and also the passthrough of global prices to core inflation.

Core inflation will remain persistently higher (3%–5%) than headline inflation throughout the entire projection period due to the robust wage growth.

In the medium term, economic activity will spur the demand for labour. Owing to this demand, the wage growth will remain persistently high (above 7%) amid labour shortage.

Such long-lasting sharp wage increases that are higher than those recorded by trade partners and that exceed productivity growth reduce the cost competitiveness and increase the risk of a weaker performance of exports.

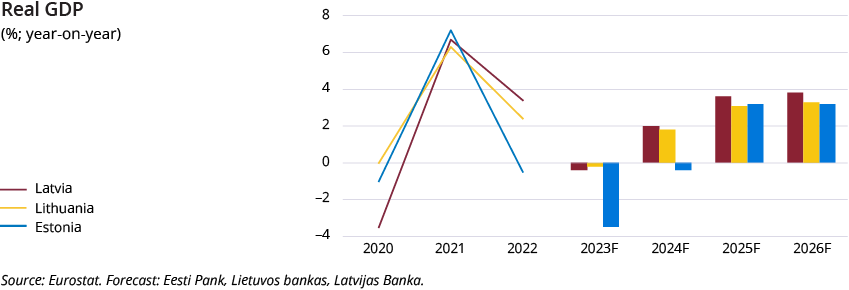

The GDP projection period can be divided into two groups:

a period of weak activity (the end of 2023 and the first half of 2024) will be followed by stronger growth (from the second half of 2024).

The downward revision of the GDP growth outlook, implying a decrease of GDP by 0.4% for this year and an increase of 2.0% for 2024, is mostly due to the revisions of the previous quarters' data by the Central Statistical Bureau of Latvia at the end of September shortly after the publication of Latvijas Banka's September forecast. However, the global geopolitical situation, the deterioration of the consumer confidence and the weak growth of the other Baltic States do not give grounds for optimism either.

- The external demand, particularly in Estonia and Lithuania, has weakened. The still restrictive monetary policy slows down the growth momentum in trade partner countries.

- The wood industry, the largest subsector of manufacturing in Latvia, is weakening further, and its price competitiveness in export markets, along with the declining demand and prices, has also worsened.

- The increase in private consumption will resume only gradually. Although the low unemployment rate, the strong wage growth and the sharp decline in inflation gradually strengthen the purchasing power of the population, the consumer confidence is significantly deteriorating. ○ Moreover, due to higher interest rates more attractive saving and investment opportunities limit consumption.

At the same time, the situation might improve in the second half of 2024 as the already growing domestic demand will also be accompanied by more rapid export growth. The GDP growth is expected to increase by 3.6% in 2025 and by 3.8% in 2026.

- Investment financed from own funds of businesses and investment co-financed by the European Union (EU) funds provide the possibility to increase production capacity, which will allow to follow the strengthening of the external demand and to supplement the export portfolio with higher value-added products.

- The role of the growth leader will be retained by investment with a significant increase in public sector demand, which, along with EU funds, will also be supported by the sizeable Rail Baltica project as well as by the planned investments in the field of internal and external security.

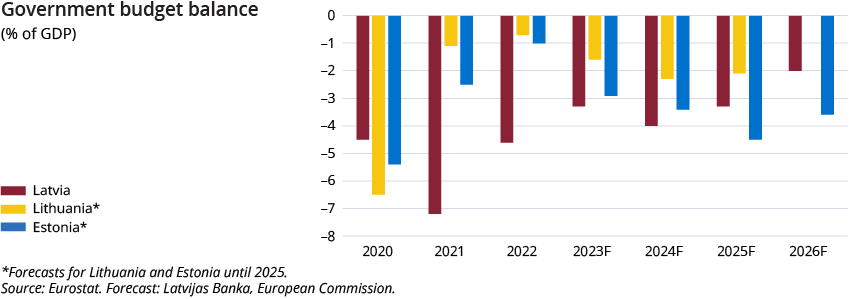

The budget for 2024 adopted by the Saeima envisages priorities in the areas significant for Latvia such as security, health and education. Additional spending and weaker economic activity are reflected in a higher government budget deficit and government debt in our forecasts. Although additional budget investment helps strengthen the resilience to geopolitical threats, an expansionary fiscal policy, at the same time, can increase the inflationary pressure and weaken the price competitiveness of the economy.

Macroeconomic fundamentals: Latvijas Banka's forecasts

|

2023 |

2024 |

2025 |

2026 | |

|

Economic activity (annual changes; %; at constant prices; seasonally adjusted data) |

||||

|

GDP |

-0.4 |

2.0 |

3.6 |

3.8 |

|

Private consumption |

-1.8 |

2.8 |

4.3 |

3.6 |

|

Government consumption |

6.5 |

0.4 |

0.5 |

0.6 |

|

Investments |

5.6 |

4.5 |

4.9 |

5.2 |

|

Exsports |

-6.2 |

-1.0 |

3.3 |

3.5 |

|

Imports |

-3.5 |

-1.0 |

3.3 |

2.7 |

|

HICP inflation (annual changes; %) |

||||

|

Inflation |

9.0 |

2.0 |

2.3 |

1.8 |

|

Core inflation (excluding food and energy prices) |

8.4 |

5.2 |

4.0 |

3.3 |

|

Labour market |

||||

|

Unemployment (% of the economically active population; seasonally adjusted data) |

6.4 |

6.3 |

6.2 |

6.1 |

|

Nominal gross wage (annual changes; %) |

12.0 |

8.0 |

7.9 |

7.6 |

|

External sector |

||||

|

Current account balance (% of GDP) |

-3.2 |

-3.6 |

-4.0 |

-3.4 |

|

Government finances (% of GDP) |

||||

|

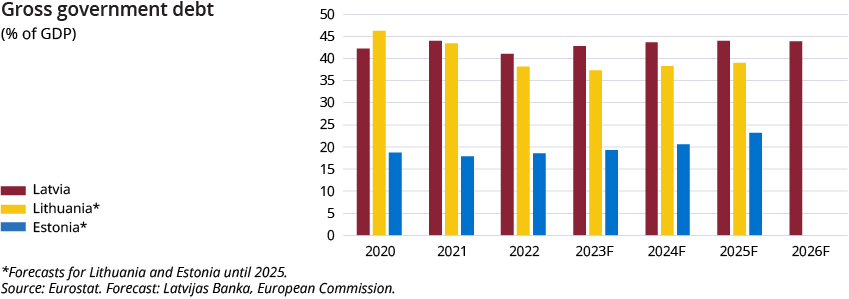

General government debt |

42.8 |

43.6 |

43.9 |

43.8 |

|

Budget surplus/deficit |

-3.3 |

-4.0 |

-3.3 |

-2.0 |

The cut-off date for the information used in the forecast is 30 November 2023, and 23 November for the information used in some technical assumptions.

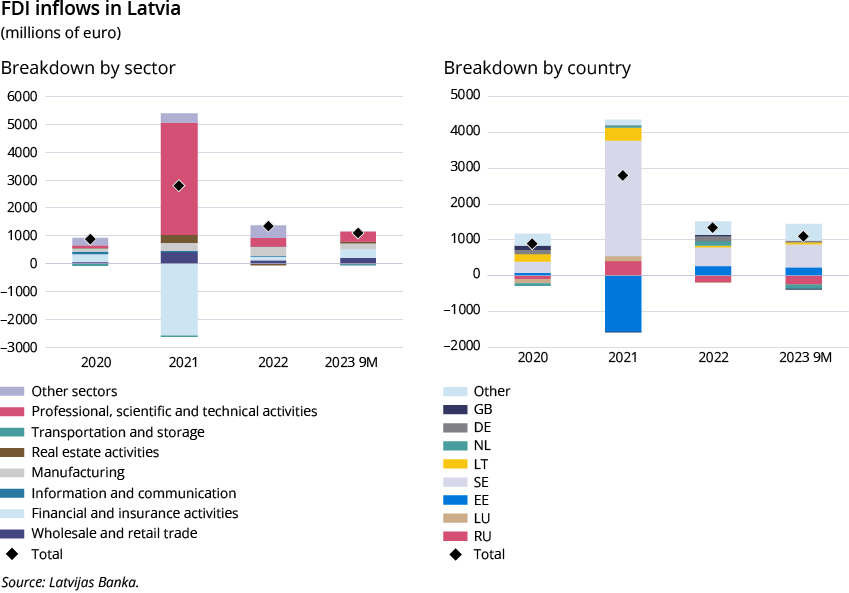

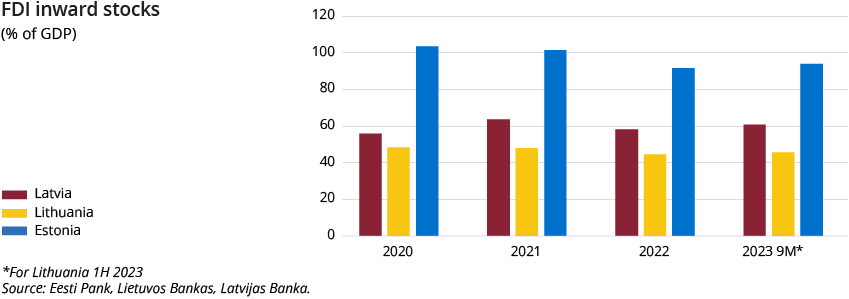

Foreign Direct Investment

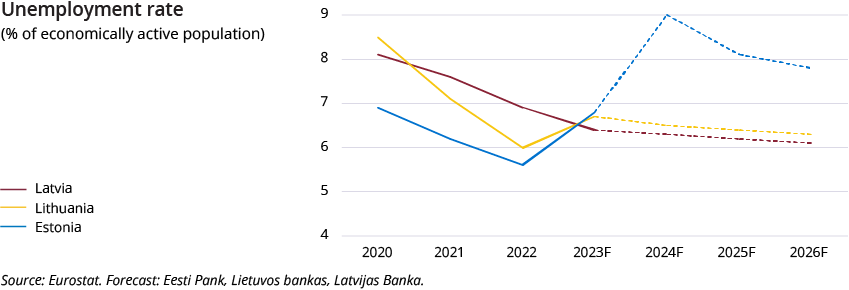

Macroeconomic Indicators: Latvia, Lithuania and Estonia

Textual error

«… …»