Latvian economy struggling to get back in the saddle

In the first quarter of 2020, Latvia's economic growth decelerated as expected on account of the weakening of external demand observed already last year, combined with several other negative factors like contracting freight transportation flows through ports and by rail and poorer performance of the energy sector, adversely affected by the warm winter conditions in the beginning of this year.

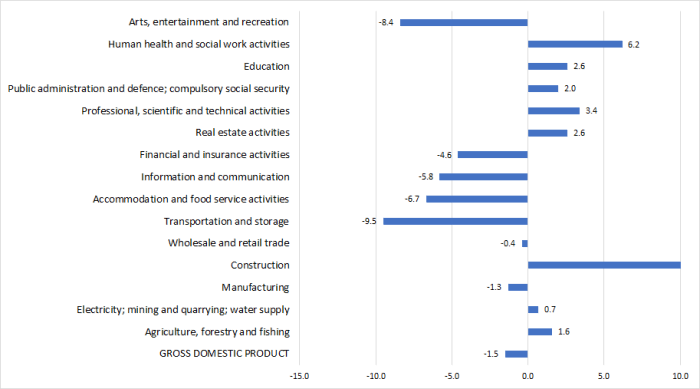

Since the beginning of February, the economy was progressively affected by the Covid-19 pandemic which gathered strength and forced governments to impose various restrictions, causing unprecedented challenges for many businesses and communities. All that has resulted in a 2.9% quarter-on-quarter decrease in the gross domestic product (GDP) in seasonally-adjusted terms in the first quarter of this year and a 1.5% year-on-year fall in both calendar-adjusted and unadjusted terms.

Hotel services, cultural, entertainment and sports events, passenger transportation, trade and other services sectors were the ones that were hit the hardest. Only some sectors have managed to wade through the first quarter without "getting their feet wet". For example, construction where the future growth prospects are also good because of investment projects supported by the government.

At the same time, there are sectors where businesses have fared quite differently in the present crisis. Looking at manufacturing, demand has decreased significantly in many product groups, while others have reached new record-highs (more detail available here). Although the global supply chain disruptions and social distancing measures had a negative effect on both wholesale and retail trade development, the rate of decrease in the case of the value added in trade was lower than that of the overall GDP. With economic sentiment deteriorating, however, the contribution of car purchases decreased, becoming negative and reaching –20% in March this year.

As to the second quarter developments, April data on retail trade suggest that, as expected, many businesses have increasingly shifted to selling products online in a state of emergency (something that was not yet obvious in March data), while the previously-seen episode of elevated demand for pharmaceutical products is over. Considering that the shopping malls were closed both over the Easter holidays and early May holidays as well as that businesses will adjust to operating in the circumstances of partial restrictions gradually, retail trade can be expected to continue to perform poorly in the second quarter.

Looking at the demand side of GDP, private consumption is accountable for almost all of the fall in the annual rate of GDP growth. This can be explained mainly by cautious behaviour in uncertain circumstances (saving for a rainy day) and some quite objective spending cuts because of cancelled entertainment, sports etc. events. Positive growth was recorded for all other expenditure components of GDP in the first quarter:

a) government consumption even increased on account of crisis support measures;

b) investment was sustained by construction activity, despite lower imports of capital goods (decreased purchases of new equipment, vehicles and other investment goods);

c) exports were underpinned by exports of goods, on account of a rise in the exports of agricultural products, sustained export flows of mechanical appliances and electrical equipment, with exports of services, however, decreasing (particularly in the sub-sectors related to tourism and transportation).

What is to be expected next? Unfortunately, most preliminary data paint quite a gloomy picture for April. At the same time, the situation is seemingly starting to stabilise in May, with some rays of sunshine breaking through the clouds both directly and figuratively. For example, following the head-dive in March-April, the economic sentiment indicators for the European Union, euro area and the Baltic States alike have shown some signs of recovery in May. Gradual lifting of restrictions and a feeling that the virus effects have been contained has resulted in people becoming more socially active and allowing themselves to buy more than the usual basic goods. So the economy is, in fact, really trying to climb back in the saddle.

At the moment, it looks that the Covid-19 effect was the gravest in March and April, with signs of a gradual stabilisation of the situation in May; hence the overall effect will be slightly smoothed out in the quarterly data. Nevertheless, the second quarter fall can be surely estimated as an even deeper one, and it is unlikely that travel and other activities will be fully restored over the summer. The probability of a new virus outbreak also remains open. There are some countries that have already started the second round in their fight against Covid-19.

It has to be admitted that, because of Covid-19, forecasting has become a bit like juggling with a slippery soap bar in the shower. Moreover, assumptions also have to be reviewed in the light of various government support measures. In addition to that, other countries prepare several economic development scenarios, with regular updates; therefore, the assumptions concerning the demand for goods and services produced in Latvia again have to be adjusted accordingly. The publication of the latest economic development forecasts of Latvijas Banka is scheduled for 5 June.

GDP growth in the first quarter of 2020 (%; year-on-year; at constant prices; calendar-adjusted data)

Textual error

«… …»

Similar articles