Krugman's Latvian Adventures

Seems like the paper by Blanchard, Griffiths and Gruss (BGG) has let Paul Krugman to admit that:

- Maybe in 2007 Latvia wasn't overvalued, just overheated;

- Then everyone (even the most ultra-Keynesian Keynesian) would call for fiscal austerity.

These were our arguments from day one. Krugman still doubts whether a particular economy can run to ~+12% output gap since textbook examples are missing. But for me it seems straightforward that small open post-transition catching-up economy such as Latvia could be much more vulnerable, and subject to larger output gaps than mature countries (based on which textbooks are written). Extraordinary circumstances that Latvia faced (just one example: credit stock to households rose by 80% y-o-y in 2006 and by another 60% in 2007) have resulted in an extraordinary overheating rarely seen (if any) before in advanced world.

This implies that 2007 is misleading base and eagerly attempts (see, for instance, here and here) to compare current economic activity (and unemployment) with 2007 level are just wrong.

If no ambiguity is left regarding the necessary fiscal policy stance during overheating, why then Latvia's fiscal policy was expansionary procyclical during the boom? First, it is unpopular to argue for headline budget surpluses given the low standards of living and first emigration wave (to higher wages) to Western Europe. However, even a small headline deficit implies a huge structural (i.e., after adjusting for the cycle) one when the economy is overheating. Second, the degree of economic overheating is usually underestimated in good times (and thus, potential output growth is overestimated) – a lesson Latvia certainly holds for other countries and the euro area in general.

So it seems that Krugman may somewhat agree on Latvia's extraordinary overheating in 2007. But Krugman is still puzzled with nominal wage "rigidity" (DNWR) during the crisis, arguing that even if this time DNWR wasn't a bidding constraint thanks to the rapid labor productivity growth, next time will be different. Let's solve Latvia's DNWR puzzle.

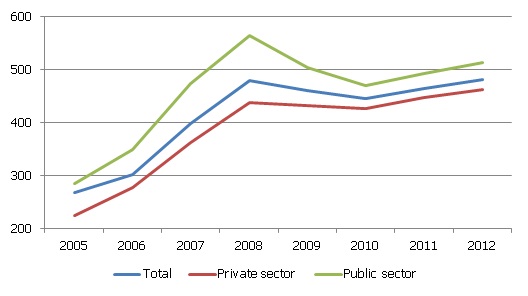

At the first glance, Latvia’s nominal wages appear rigid; especially in the private sector (see Figure 1).

Figure 1. Latvia’s average monthly gross wage for full-time job (LVL)

Source: Central Statistical Bureau of Latvia

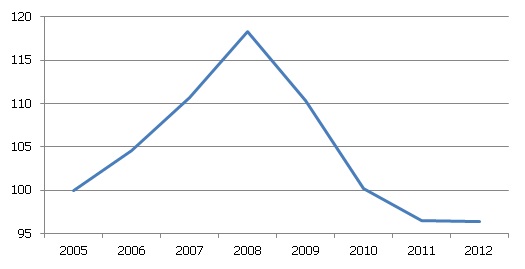

Hence, given the full adjustment of unit labor cost (ULC) (see Figure 2) this implies a leading role of labor productivity growth in Latvia’s ULC adjustment; and that puzzled both Krugman and BGG.

Figure 2. Latvia’s real unit labor cost index (2005 = 100)

Source: Eurostat

Krugman suggests this is indication of DNWR. As for me, wages in Latvia are very flexible (as both collective bargaining and trade union density rates are one of the record low in Europe), while Figure 1 reflects a bias of average wage statistics. The two sources of such bias are the hoarding of qualified labor and the decreasing length of average working week during the crisis.

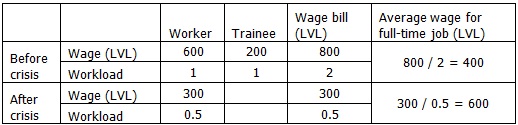

Let's see what Latvia's average wage dynamics actually means. Suppose before the crisis a particular company employed a worker and a trainee for a monthly pay of 600 and 200 lats respectively (consequently, the average wage in this company amounted to 400 lats). With the onset of crisis, the trainee was fired and the worker was shifted to a part-time job, thus "the average wage" (actually the average pay for full-time job)... rose to 600 lats (see Table 1). Actual income fell for both employees, but average wage rose. As there were many companies in Latvia that hoarded qualified labor and fired less skilled employees (increasingly employed during the past economic boom), and there was large decline in the average working week length, there is no wonder why "average wage" looks so "rigid". And as layoffs were particularly high in the private sector (for instance, number of occupied posts between 2007 Q2 and 2010 Q1 decreased by 52% in construction, 36% in manufacturing, 32% in trade in a seasonally adjusted terms), so does the labor structural changes; therefore, there is no surprise that private sector's "average wage" appears to be so "rigid".

Table 1. Calculation of average wage for full-time job (an illustration)

Textbook examples of nominal wage rigidity intrinsically assume workload and employee's average quality to remain constant. This assumption however does not hold under extraordinary economic circumstances, such as experienced by Latvia recently.

Concluding, Krugman is gradually getting closer to the arguments we have presented from the outset. Moreover, I have one thing to add to Krugman's post and BGG paper: nominal wages in Latvia are in fact rather flexible. If this remains, it will surely help in future adjustments (which hopefully though, will not be as dramatic as the last one).

Textual error

«… …»