Waves in the sea go up and down – one. Waves in the sea go up and down – two? Rhyme on Latvia's GDP

A month ago, the previous series of the GDP flash estimate revealed that the second quarter saw Latvia's economy shrink relatively significantly, i.e. by 7.5% quarter-on-quarter. At the same time, the contraction was less dramatic than in other EU countries. This series or specified GDP production and expenditure components reveal a more detailed picture of the "culprits" driving the change. Moreover, they show that GDP contracted by 6.5%, i.e. less than previously expected.

In light of the current news, the basic principles of logic and various preliminary data, we already had an idea of the "culprits". For instance, border restrictions clearly hampered international transport and travel in particular. As a result, Latvia saw much less tourists during this period.

Meanwhile, the extent to which the tourism sector was affected by the local travellers and those from the closest neighbouring countries was less apparent and had to be guessed in many instances. Indeed, how long can one lie on the couch, do cross stitch embroidery and renovate the terrace? This summer, I observed that many regional tourism objects drew larger crowds than those you would normally see on Brīvības Street. At the same time, the capacity utilisation rates of the largest conference halls, sport arenas, cultural venues and hotels fell dramatically, and the overall expectations for the services sectors were grim.

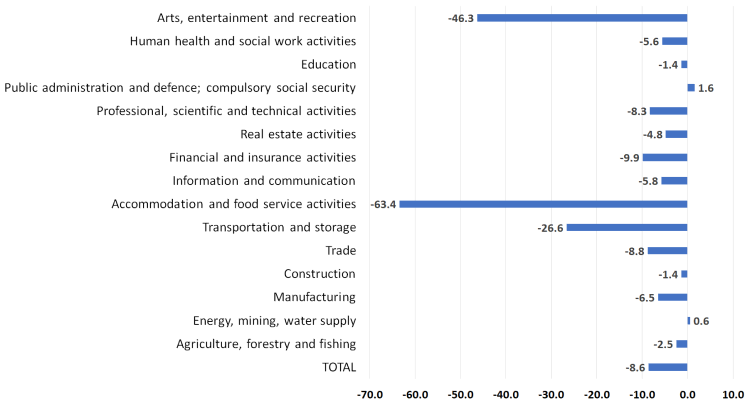

Among the services sectors, those servicing domestic demand – trade (most likely, retail trade), education, health care and public administration – suffered less. The contraction in the information and communication services sector was also relatively insignificant since this sector was critical in ensuring remote processes. As was expected, the sectors of arts, culture, accommodation and transport reported the steepest declines due to limited spending or lower passenger flows.

Looking at GDP by expenditure, the estimated investment results were less positive than in the first quarter. Moreover, in addition to the previously observed dynamics of contracting imports of capital goods, the performance of the construction sector also worsened in the second quarter. Nevertheless, in the third quarter the construction output is expected to increase as it will be facilitated by the financing from EU funds and the government support to mitigate the negative impact of the COVID-19. Overall, the government's COVID-19 measures will continue to promote investment. Moreover, in the coming years significant support will be made available via the Next Generation EU recovery plan which will allow Latvia and the EU overall to foster the development after the hardships of the crisis.

Private consumption shrank surprisingly rapidly in the first quarter. Besides, the contraction in private consumption was much more pronounced than the decline in household income. The accumulation of savings and the postponed consumption suggested that the decline may have been less steep in the second quarter. However, it turned out to be significant: more than one fifth lower year-on-year. The decline was inevitable as part of the planned spending was never carried through, i.e. more distant travels as well as cultural and sporting events were postponed. Moreover, many households received significantly lower income, although at least part of the lost income was compensated by the government support as well as unemployment and furlough benefits. Nonetheless, the income decline seems to be too steep. Furthermore, the decrease in the household spending on utilities, mostly water, electricity, gas and other fuels, is also puzzling: during the period of restrictions, with many people working and studying remotely from home, such consumption should have grown.

With a dramatic fall in the volume of services exports and a less substantial decline in exports of goods, the dynamics of exports paint a picture similar to that of the sectoral structure. Foreign trade data also suggest a steep decline in the volume of exports of individual groups of goods associated with re-exports (e.g. transport vehicles).

As to the economic outlook for the third quarter, there is good reason to expect better results due to more relaxed COVID-19 restrictions and overall more positive sentiment among consumers and businesses. This was confirmed by the August sentiment indicators which were published a few days ago and, once again, suggested an improvement.

Overall, the situation is more positive than estimated in some versions of the spring projections. However, there is no room for complacency as the probability of repeated virus outbreaks is relatively high. In some countries, the fight against the virus is already becoming increasingly more fierce, and some of them are very close to us (e.g. our neighbour Lithuania). With the borders remaining open, the waves swelling and splashing around the boats of the neighbouring countries will sooner or later roll over and rock the boat of Latvia as well. Waves in the sea go up and down – one. Waves in the sea go up and down – two? Nevertheless, with less restrictions on international travel and the availability of more virus treatments, which would be created in the meantime, the scenario of a second wave will most likely play out differently than in the spring. If, however, you, once again, find yourself looking for new ways to entertain your children, you can teach them the rhyme "Waves in the Sea".

GDP growth in the second quarter of 2020 (%; year-on-year; at constant prices; calendar-adjusted data)

Textual error

«… …»