Uncertainty weighs on spending

Three months spent in a lockdown have resulted in a considerable deterioration of the economic environment and have had negative repercussions in almost all sectors of the economy. With the COVID-19 outbreak starting to subside and the economic activity gradually recovering, we can now look back at the developments in the monetary aggregates over the most recent months. Actually, the pace has remained steady and the crisis has had no significant effect on either the amount of deposits received, or that of the loans granted. This leads to two main conclusions:

- the uncertainties surrounding the future success in limiting the virus spread and the ability of the economy to adapt to the new circumstances have made households cut back on their consumption significantly and increase savings. That (along with export limitations) has really decreased the saving opportunities for businesses; nevertheless, the deposits placed with banks have overall grown over the last three months;

- given the current sentiment of consumers and banks, the lending portfolio has shrunk, but not to a significant extent and the rate of decline is not much different from the one observed in the months before the crisis. Although banks have become more prudent when setting the credit standards and evaluating the creditworthiness of their borrowers, this effect was partly offset by the high degree of the monetary accommodation and a flexible approach to the existing loan commitments pursued by the banking sector.

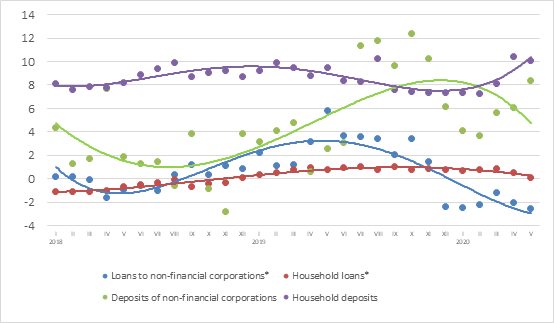

Domestic deposits increased by 3.6% from March to May, with household deposits growing by 3.8% and deposits by non-financial corporations merely increasing by 0.4%. As a result, the annual growth rate of domestic deposits was 10.7% in May, with the respective rates in the household and non-financial corporation sectors standing at 10.1% and 8.4% respectively. Against the background of turbulent global financial markets, deposits by non-bank financial institutions with Latvian banks have recorded particularly high growth rates: 21.1% in three months, mostly on account of pension funds.

At the same time, the domestic loan portfolio contracted by 0.2% over the same period, with loans to non-financial corporations edging up by 0.3% and the loan portfolio of households remaining broadly unchanged. Lending to non-bank financial institutions was the only category reporting a decline in the course of three months, shrinking by 2.0%. The annual rate of change in domestic loans (excluding the impact of the restructuring of the banking sector and the reclassification of institutional sectors) became increasingly more negative: –2.3% for loans overall and –2.5% for loans to non-financial corporations in May. A marginally positive annual growth rate was still reported only in lending to households (0.1%). Although the months of the crisis had virtually no effect on the size of the loan portfolio, the impact on new loans was quite obvious in April and May. The amount of renegotiated loans grew significantly over those two months, whereas that of new loans considerably decreased, with the average monthly amount being just 45 million euro in the case of households (73 million euro in 2019) and 48 million euro in the case on non-financial corporations (84 million euro in 2019).

Annual changes in domestic loans and deposits (%)

Source: Latvijas Banka

*For the sake of comparability, the one-off effects related to the restructuring of Latvia's banking sector and the reclassification of the institutional sectors have been excluded.

Textual error

«… …»