Manufacturers shift into a higher gear, yet the roads are bumpy to Madona and Rome alike

The economic sentiment indicators were the first ones to signal an improvement in Latvia, suggesting that the optimism of traders and manufacturers as well as consumers with regard to the current state of play and the future has grown since May.

A week ago, a surprisingly impressive improvement was shown by the May data on retail turnover, meaning that life is returning to shops and people are venturing outside their homes more often and spending more.

The hopes were high for manufacturing data, where an improvement was suggested already by the previous industrial confidence data. Not as high as in the case of retail trade, however, because, in addition to the spending of the local population, manufacturing is also more strongly affected by exports.

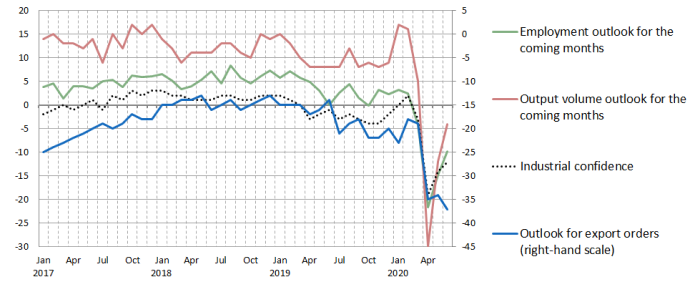

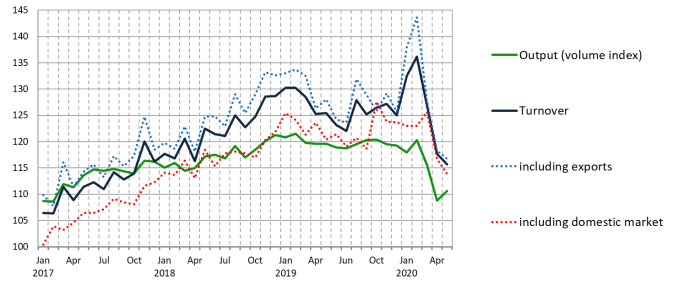

The development of exports was less predictable, as the industrial confidence data showed no improvement for the outlook for export orders and even a fall in June (see Chart 1). Julius Caesar has once said that he would rather be the first in a village than the second in Rome. Considering the market potential, profitability, capacity and productivity building opportunities, manufacturers cannot be advised to follow Caesar's advice. Even if there is a more robust recovery in the village or the domestic market at the moment (not quite confirmed by the turnover data published today; see Chart 2), this is just temporary and foreign markets will eventually provide wider opportunities. It's not by chance that the long-term growth of export turnover is steeper, and at the beginning of the year exporters had managed to get quite far on their road to Rome and other foreign markets. Let's note that the improvement in the volume index and the decline in turnover shown in Chart 2 should not be viewed as a controversy, because it is explained by the fall in producer prices.

Naturally, not everything produced can be exported. There are different expiry dates, transportation costs and other economic considerations involved. Moreover, exports may be decelerated by weaker aggregate foreign demand as other countries also are going through the crisis, the fact that the goods we are producing are, at the moment, not what buyers need most (for example, not a lot of cars are sold in a period of crisis, hence the car parts we are producing are also not in high demand), changes in price competitiveness and various other factors.

What else is interesting when looking at the demand for goods? The panic buying of canned fish, buckwheat and pasta is over, and the situation in food production is gradually normalising, returning to the pre-virus levels of capacity and demand.

Nevertheless, there are also some areas sustained by new habits and ideas. For instance, the "Do-It-Yourself" segment remains strong, with people in Latvia and elsewhere paying increasingly more attention to various housing renovation and improvement issues. Consequently, the manufacturers and traders offering products like wood, furniture fittings, paints etc. have no reason to complain about lack of demand.

While certain borders remain closed and travelling is limited, people will keep themselves more busy at home, trying to increase the level of comfort in their dwellings or create additional recreation facilities: a sauna is built, a new fishing boat is equipped or a loom for weaving is installed.

June is likely to witness a further improvement in this area. Government support will still be important for manufacturers, as, given the depth of the fall and the uncertainty surrounding the global impact of the virus, it is too early to believe that we have already put the crisis behind us.

Chart 1. Industrial confidence indicator and select survey questions (%)

Chart 2. Manufacturing output (volume index) and turnover (2015=100%)

Textual error

«… …»