On macroeconomic forecasts by Latvijas Banka. June 2020

Latvijas Banka has revised its gross domestic product (GDP) and inflation forecasts for Latvia.

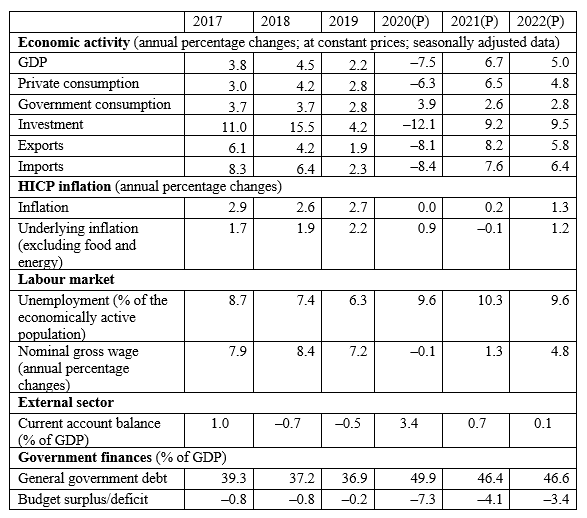

In the light of the latest global economic developments, including the implications of the COVID-19 pandemic, Latvijas Banka has revised its projections for Latvia's GDP growth in 2020 downwards from –6.5% in its March forecasts to –7.5%, and inflation projections from 0.5% in March forecasts to 0%. Economic growth is expected to rebound to 6.7% in 2021, while inflation will edge up to 0.2%.

The COVID-19 pandemic has had a negative effect on global economic growth. Although the outbreak is past its peak and several countries already have plans for a gradual jump-start of their economies, the uncertainties surrounding the duration and extent of further restrictions to limit the virus spread and the ability of the economies to adjust to the new circumstances remain high. Central banks and governments have responded actively to the crisis by implementing monetary and fiscal policy support measures.

International institutions project a decrease in the global GDP in 2020. The euro area has also already recorded a drop in economic activity in the first quarter, and the fact that the economic sentiment indicators have fallen to their historical lows signals an even deeper plunge in the second quarter.

According to Latvijas Banka assessment the economic environment has deteriorated since the publication of its March forecasts. The most recent forecasts factor in an extension of the state of emergency until 9 June and a longer duration of the precautionary measures to limit the spread of COVID-19, even though part of the measures are being lifted gradually. A modest result was recorded for Latvia's GDP in the first quarter, industrial confidence indicators deteriorated significantly and the outlook for external demand is also weaker than at the onset of the COVID-19 crisis. Therefore, Latvijas Banka has revised its GDP projections for 2020 downwards from –6.5% in its March forecast to –7.5% in its June forecast.

The updated forecast suggest that the restrictions imposed in the field of services (cancellation of public and private events) and travelling bans have a considerable downward effect on consumption, affected also by falling incomes. The uncertainty surrounding the gravity and duration of the consequences of the COVID-19 pandemic has resulted in a more cautious spending behaviour of households; therefore, the fall in consumption is estimated to be deeper than that in disposable income. Services exports are affected heavily as tourist flows and passenger transportation by air ceased due to the imposed state of emergency restrictions. At the same time, a broad-based weakening of activity in external markets reduces exports of goods.

Investment is expected to shrink significantly in 2020. Despite the favourable effect of the government's decisions to increase public investment, the high degree of uncertainty will act as a limiting factor to new private investment.

The government's crisis support measures to businesses and households and the planned public investment to stimulate the economy have pushed the fiscal deficit above 7% of GDP (the cut-off date for fiscal measures included in the present forecast is 25 May). The European Commission has relaxed the fiscal deficit rules in this crisis, allowing flexibility in addressing the crisis consequences, to the extent that it does not undermine the sustainability of public finances. At the same time, the government can provide significant support, as, during the present crisis, Latvia is able to borrow in external markets, increasing the government debt to close to 50% of GDP.

Assuming a gradual recovery of the economy as of the second half of 2020, Latvijas Banka projects a 6.7% GDP growth in 2021. This scenario, however, expects that the recovery of the economic activity, following significant restrictions as well as demand and confidence shocks, will be uneven, failing to reach the levels projected before the crisis over projection horizon, i.e. by 2022 and returning to the pre-crisis level at the end of 2021, with significant differences across sectors.

Data suggest that construction was one of the sectors where growth was affected less in the first quarter. Moreover, the sector will be further underpinned by the government's investment support measures. Demand for basic goods (for example, agricultural products) can be expected to remain more resilient. The need for new IT solutions is also anticipated. These factors could support activity in the above-mentioned sectors.

At the same time, the sub-sectors relating to hospitality services and cultural and entertainment events with large attendances are expected to resume growth only gradually with household caution persisting. The recovery of the transport sector will be additionally hampered by earlier factors, unrelated to the COVID-19 pandemic. Therefore, the growth of those sectors is expected to recover more slowly and undershoot the previous levels longer.

Inflation retreated below 0% in April and May, as a result of both the effect of the oil price dives on fuel and heating prices and more moderate services price developments due to the measures to limit the spread of COVID-19. According to Latvijas Banka projections, the annual inflation will linger around 0% in 2020 and 2021 (0.0% and 0.2% respectively). The projections have been revised slightly downwards in comparison with the March forecast, as the oil prices remained at low levels longer than expected.

The restrictive measures to fight the COVID-19 pandemic had an immediate effect on the labour market as businesses were forced to downsize. The increase of unemployment, however, is expected to be lower than during the previous global financial crisis, as the government provides crisis support to businesses and individuals. Because of the low economic activity, businesses have to consider cost optimisation solutions and consequently also the ways of reducing their labour costs. Moreover, labour availability is growing on account of rising unemployment and therefore unlikely to exert an upward pressure on wages even after the economy has started recovering, thereby hindering increase in prices next year as well.

Macroeconomic fundamentals: actual data and Latvijas Banka projections (P)

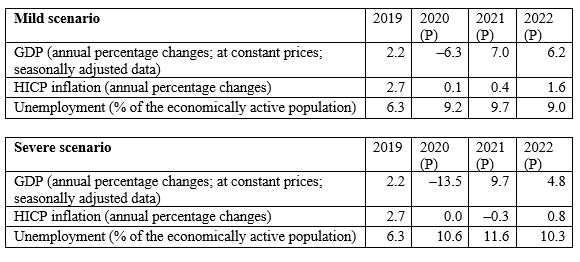

In addition to the baseline scenario of the forecast, Latvijas Banka economists have separately evaluated the effects of both mild and severe development scenario on the economy.

The significant Eurosystem's monetary policy support and fiscal policy support provided by governments help to mitigate the economic consequences of the COVID-19 pandemic at the height of the crisis as well as provides a strong economic recovery stimulus after the crisis. A substantial additional support is provided by the updated proposal of the European Commission on the next EU long-term budget and the recovery fund that would allow to draw additional financing to stimulate the economies of the Member States and improve the future outlook of investors. Under this scenario, a reduced spread of COVID-19 in Europe and easing of the current precautionary measures both domestically and abroad would increase the degree of household optimism and enable a speedier recovery of consumption, depleting precautionary savings built up at the beginning of the crisis unlocking the pent-up demand. A speedy and successful containment of the COVID-19 pandemic as well as the use of effective support instruments would allow to project a smaller GDP decline in 2020 (–6.3%) and a swift economic recovery in the subsequent years in the mild scenario.

At the same time, the baseline scenario of the economic growth forecasts does not include a second wave of the virus spread. Nevertheless, should COVID-19 restart spreading after the social restrictions are gradually lifted and should there be no medical remedy available yet, tight restrictions would need to be renewed and vigorously imposed. According to this severe scenario of Latvijas Banka, GDP would decrease by 13.5% this year and the economic recovery would also take longer, with no return to the pre-crisis levels seen over the forecast horizon (up to 2022).

Even if the society had already partly adjusted to living in the "new normal" and the economic implications of the restrictions were less significant than at the start of the state of emergency, the elevated uncertainty surrounding the future prospects would cause considerably stronger confidence and demand shocks for economic agents.

More cautious behaviour of households and investors would weaken and postpone the recovery of consumption and investment even more, while the affected businesses would have to review their expenses, including labour costs, more considerably. Less investment and higher structural unemployment would also weaken the economic potential in the medium-term.

Macroeconomic fundamentals: actual data and Latvijas Banka projections (P)

The cut-off date for the information used in the forecast is 25 May 2020.

Textual error

«… …»