Latvia's Macro Profile. September 2023

Inflation is declining in the euro area and Latvia; however, the world's major central banks have emphasised that inflation will remain above the target level over a longer period:

- the euro area inflation forecasts for 2023 and 2024 have been revised up in September, and only those for 2025 have been revised down, reaching the average level of 2.1% in the last forecast year;

- to ensure the return of inflation to its 2% target in the medium term, the Governing Council of the European Central Bank (ECB) continued to raise its key interest rates. At its September meeting, it decided to raise its key interest rates by another 25 basis points, with the rate of deposit facility, which banks may use to make overnight deposits with the Eurosystem, reaching 4%;

- The ECB's Governing Council considers that the key ECB interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the monetary policy target (2%).

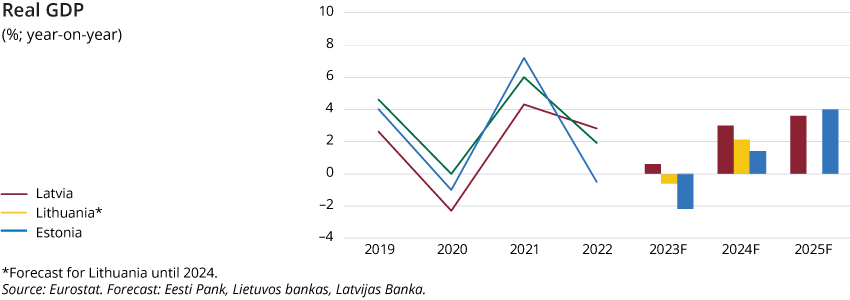

The forecasts were revised on account of lower than expected GDP growth in the second quarter of 2023 and a slightly changed outlook for the following years, but revisions of historical data also play a significant role in GDP components:

- the persistently high inflation had adverse effects on purchasing power and consumption;

- activity of several sectors, such as manufacturing and agriculture, fell from unusually high levels;

- commercial banks point to tighter credit standards and weaker demand for credits;

- the outlook for foreign demand and export opportunities deteriorated slightly;

- natural processes (heat, storms, rainfall, bark beetle damage) have adverse effects on the quality and price of timber and grain – two important commodity groups in exports.

However, economic activity might recover gradually by the end of this year, as household purchasing power is expected to recover and investments are projected to follow an upward trend:

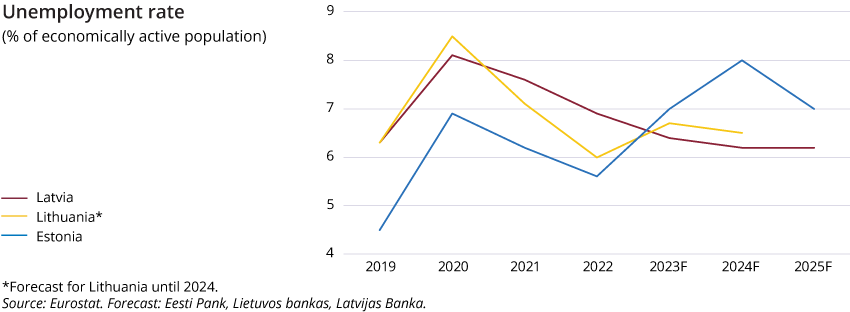

- falling inflation along with a strong wage growth will gradually strengthen the household purchasing power. Irrespective of the economic slowdown, the unemployment rate remains low; moreover, the labour market experiences labour shortages;

- the support measures planned by the government will also strengthen the household purchasing power. Compared with the previous heating season, the government expenditure foreseen for these measures has been reduced; however, the measures are more targeted;

- sentiment among economic agents and firms' employment expectations are starting to improve gradually;

- the implementation of investment projects to be finished by the end of the year according to the financing terms of the European Union funds will maintain investment activity.

Inflation is falling further, with the previously observed supply-side constraints waning:

- global resource prices and commodity import prices have fallen – energy prices are lower than a year ago, global food prices have drifted downwards over the past months;

- producer prices in manufacturing are declining, and they have already fallen below the level reached last year, largely reflecting the energy price adjustment;

- the expected heating prices in most of Latvia are lower than during the previous heating season;

- the price expectations have decreased significantly among consumers and firms;

- however, there are risks of price rises and, for example, global markets have seen a rebound in oil prices recently; the impact of increasing wages on prices is also intensifying.

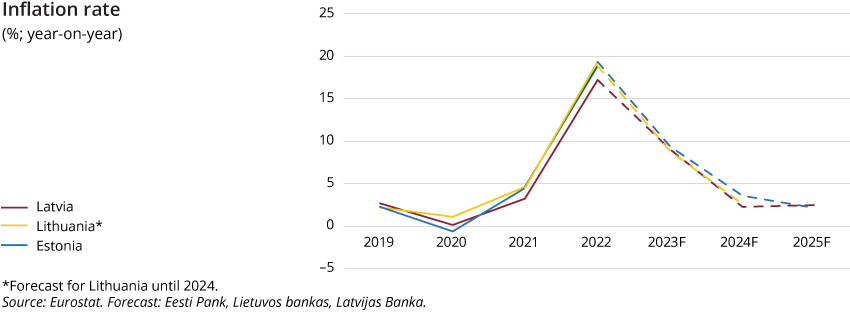

The most recent inflation data point to a stronger-than-projected rise in prices of energy, services and industrial goods. Thus, the inflation forecast for 2023 has been revised up to 9.0% (the June forecast – 8.5%). At the same time, the core inflation is expected to remain elevated in 2023 and beyond due to the strong wage growth affecting both demand and costs in the price-setting process.

Meanwhile, assumptions about lower food and natural gas prices allow for downward revisions of inflation forecasts for the next years: to 2.3% for 2024 (the June forecast – 2.4%), and to 2.5% for 2025 (the June forecast – 3.0%). The core inflation will decrease more gradually from 8.2% in 2023 to 4.2% in 2025.

To sum up, inflation is declining rapidly, and economic activity will recover and accelerate despite its sluggish state. The current steep wage rise that exceeds inflation alleviates the financial position of households, and gains in purchasing power contribute to economic activity. However, firms have the capacity to raise wages of their employees rapidly for an extended period of time only if their productivity also increases buoyantly. Therefore, the rapid wage growth, which contributes to a short-term rebound in purchasing power, can impair competitiveness.

Macroeconomic fundamentals: Latvijas Banka's forecasts

|

2023 |

2024 |

2025 |

|

|

Economic activity (annual changes; %; at constant prices; seasonally adjusted data) |

|

||

|

GDP |

0.6 |

3.0 |

3.6 |

|

Private consumption |

–0.5 |

4.0 |

4.4 |

|

Government consumption |

4.3 |

0.2 |

0.4 |

|

Investments |

6.0 |

4.9 |

5.7 |

|

Exsports |

–1.7 |

2.1 |

3.1 |

|

Imports |

–1.9 |

1.8 |

3.4 |

|

HICP inflation (annual changes; %) |

|

||

|

Inflation |

9.0 |

2.3 |

2.5 |

|

Core inflation (excluding food and energy prices) |

8.2 |

5.3 |

4.2 |

|

Labour market |

|

||

|

Unemployment (% of the economically active population; seasonally adjusted data) |

6.4 |

6.2 |

6.2 |

|

Nominal gross wage (annual changes; %) |

12.0 |

8.2 |

7.8 |

|

External sector |

|

||

|

Current account balance (% of GDP) |

–3.1 |

–3.5 |

–3.9 |

|

Government finances (% of GDP) |

|

||

|

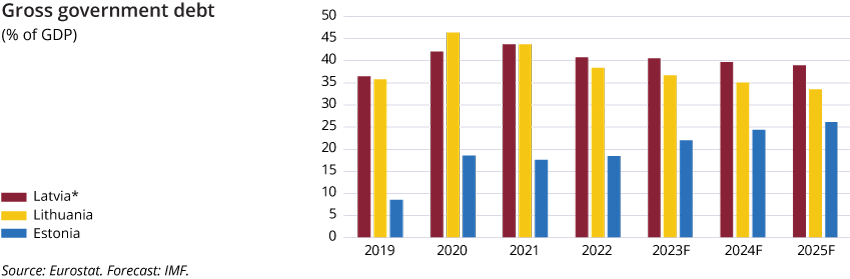

General government debt |

42.0 |

41.6 |

40.9 |

|

Budget surplus/deficit |

–3.3 |

–3.0 |

–1.7 |

The cut-off date for the information used in the forecasts is 15 September 2023 and 22 August for the information used in some technical assumptions.

Textual error

«… …»