Latvia's Macro Profile. March 2023

Latvijas Banka has published its latest March 2023 macroeconomic forecasts drawn up amid persistently high uncertainty.

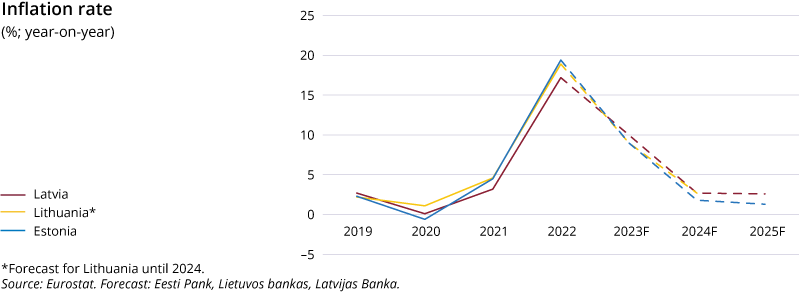

- The inflation forecast has been revised downwards for the entire projection horizon: to 10.0% for 2023 (10.9% in the December 2022 forecast), to 2.7% for 2024 (4.4%) and to 2.6% for 2025 (3.0%).

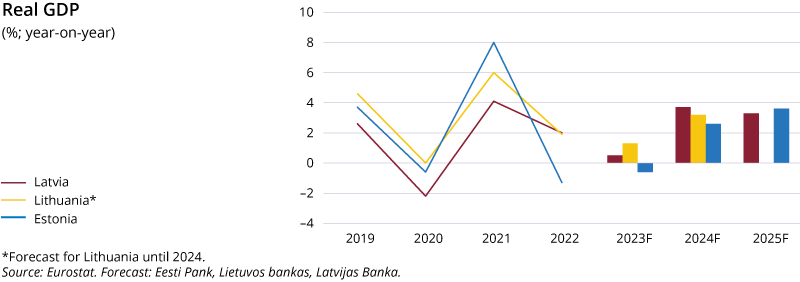

- The gross domestic product (GDP) growth forecast for 2023 has been revised upwards to 0.5% (a 0.3% fall was projected in December) which in turn reduces the GDP growth in the coming years: to 3.7% for 2024 (a 4.4% rise was projected in December) and to 3.3% for 2025 (3.5%).

- Inflation in the euro area remained significantly above the central bank target (2% in the medium term). Although it has currently reached its peak and follows a downward trend, it is expected to stay above the target for too long. Therefore, the central bank will continue acting within the scope of its mandate as long as it returns to its target.

- To ensure the return of inflation to its 2% target in the medium term, the Governing Council of the ECB is raising interest rates. In March, it was decided to increase the interest rates by another 50 basis points.

- The Governing Council of the ECB closely follows the information on tensions in the financial sector and is ready to use the instruments at its disposal to maintain price stability and financial stability.

- The euro area banking sector is resilient, with strong capital and liquidity positions. In any case, there are enough instruments at the disposal of the Governing Council of the ECB and the Eurosystem (comprising the ECB and the national central banks of the euro area) to provide liquidity support to the financial system and ensure the smooth transmission of monetary policy.

- Inflation in Latvia remains high – it was the highest among the euro area countries in February.

- Due to falling global commodity prices, inflation in Latvia will also gradually subside over the course of 2023 and could fall below 3% at the end of the year.

- Average annual inflation will still be high in 2023 (10.0%); however, it could already end up below 3% in 2024–2025.

- Lower energy prices also have a favourable effect on core inflation by reducing production costs of goods and costs of providing services; nevertheless, it will remain relatively high.

- Although the impact of wage increase on core inflation has so far been assessed as minor, a stable rise in wages and subsequent pressure on core inflation are projected in the context of labour shortage.

- Wage growth was moderate, and this year, it will be supported by an increase in the minimum wage. However, the elevated inflation will continue to reduce the population's purchasing power.

- Amid the high inflation, government support provided significant help to the population, especially in covering energy costs. Savings accumulated during the pandemic also let part of the population keep their consumer behaviour unchanged.

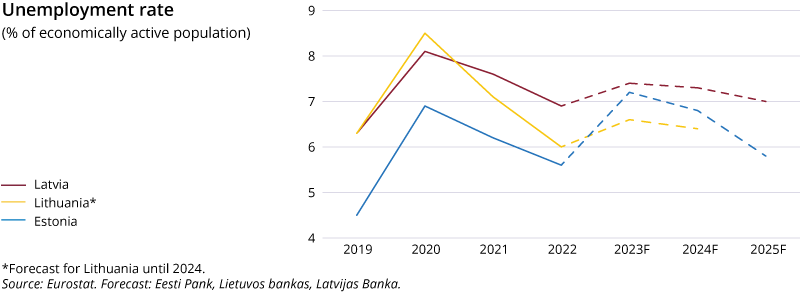

- With businesses facing weakening demand and climbing costs, labour demand declined somewhat – the number of job vacancies decreased.

- However, the projected short-lived recession and the expected labour shortage resulting from the rebound in activity make businesses retain their employees, and there is no significant change in the unemployment rate.

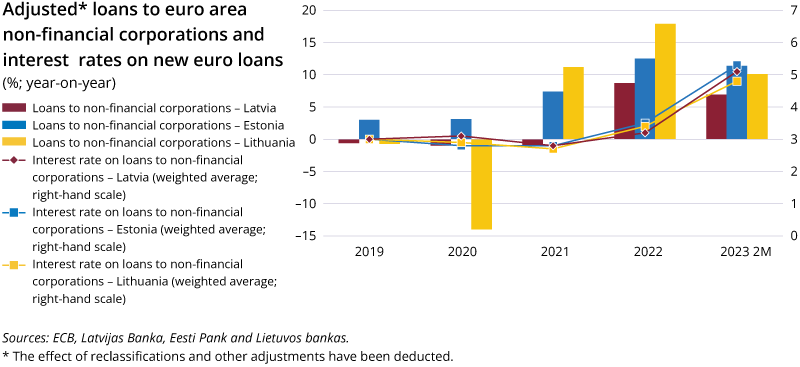

- At the same time, the investment growth prospects have not improved, taking into account the sluggish absorption of European Union (EU) funds as well as the elevated uncertainty and rising interest rates weakening the slow lending.

The most significant risks to Latvia's economic growth involve the persistently low investment level and deteriorating competitiveness. Following the steep rise over the previous years owing to a favourable exports structure, Latvia's global export market share remains resilient. Nevertheless, due to the accumulated input costs, exports could lag behind foreign demand. In the long term, investment is a precondition for a competitive economy.

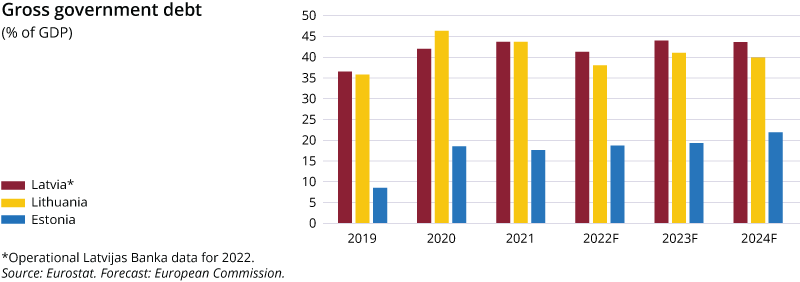

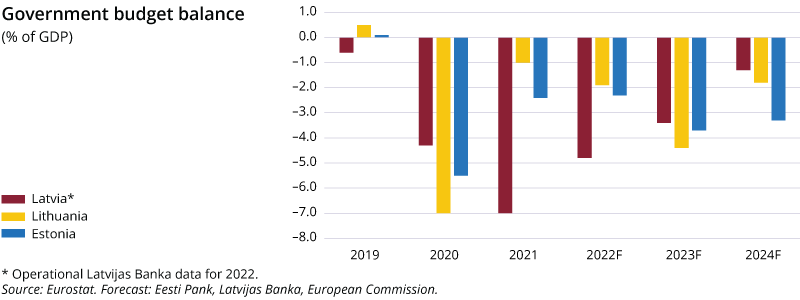

The general government deficit (4% of GDP this year) could decrease in the future; however, efforts related to facilitating economic transformation are relevant. The full absorption of EU funds as well as an improved quality and availability of public services are important aspects.

Macroeconomic fundamentals: Latvijas Banka's spring 2023 forecasts

|

2023 |

2024 |

2025 |

|

|

Economic activity (annual changes; %; at constant prices; seasonally adjusted data) |

|

||

|

GDP |

0.5 |

3.7 |

3.3 |

|

Private consumption |

0.7 |

4.2 |

4.1 |

|

Government consumption |

–2.0 |

0.5 |

0.8 |

|

Investment |

0.8 |

5.1 |

6.0 |

|

Exports |

–0.4 |

2.9 |

3.3 |

|

Imports |

–4.3 |

3.0 |

4.1 |

|

HICP inflation (annual changes; %) |

|

||

|

Inflation |

10.0 |

2.7 |

2.6 |

|

Core inflation (excluding food and energy prices) |

7.7 |

5.8 |

4.8 |

|

Labour market |

|

||

|

Unemployment (% of the economically active population; seasonally adjusted data) |

7.4 |

7.3 |

7.0 |

|

Nominal gross wage (annual changes; %) |

9.1 |

8.8 |

7.8 |

|

External sector |

|

||

|

Current account balance (% of GDP) |

–2.8 |

–3.2 |

–3.8 |

|

Government finances (% of GDP) |

|

||

|

General government debt |

41.6 |

40.0 |

39.8 |

|

Budget surplus/deficit |

–4.0 |

–2.7 |

–1.5 |

c

c

Textual error

«… …»