Latvia's Macro Profile. October 2020

Latvia's Economic Developments and Outlook

Latvia's experience in overcoming the COVID-19 crisis

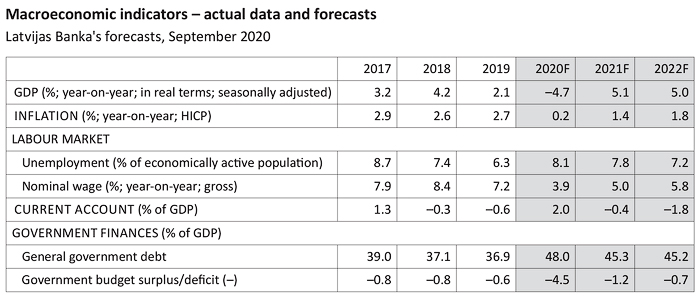

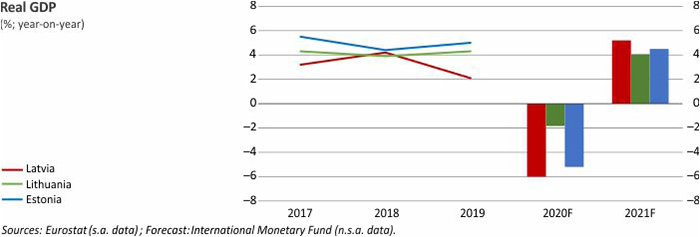

So far, Latvia's economy has weathered the COVID-19 crisis better than most European Union (EU) countries. Over the second quarter of 2020, Latvia's GDP fell by 7.1%, i.e. less than previously projected by Latvijas Banka. Factors such as balanced economic growth and sound government finances before the crisis, accommodative monetary and fiscal policy implemented already at the outset of the crisis as well as timely unwinding of the pandemic-related restrictions supported an improvement in the market participants' sentiment and, in the summer, led to a rapid recovery of several economic sectors like retail trade, manufacturing and exports of goods. These developments give reason to anticipate a less pronounced fall in GDP in 2020 (–4.7%) than estimated in the first half of the year. At the same time, uncertainty about the global development remains high.

The impact of the pandemic on sectors

A number of sectors, tourism and transportation services by air in particular, are still affected by weaker demand and increased consumer cautiousness caused by the pandemic. Nevertheless, improvement in the economic sentiment and investment growth is expected to be supported by the financing provided to the Member States under the Next Generation EU recovery plan agreed among EU leaders. The projected strengthening of external demand will improve the prospects of manufacturing and exports. Meanwhile, the purchases – those of durable goods in particular – that were postponed during the crisis will support the recovery of retail trade and private consumption. These developments give reason to anticipate around 5% growth in both 2021 and 2022. Information and communication services whose contribution to services exports has tripled since the previous crisis (15% in 2019) could retain growth duethe strong demand for information technology solutions triggered by the crisis.

Labour market and inflation forecast

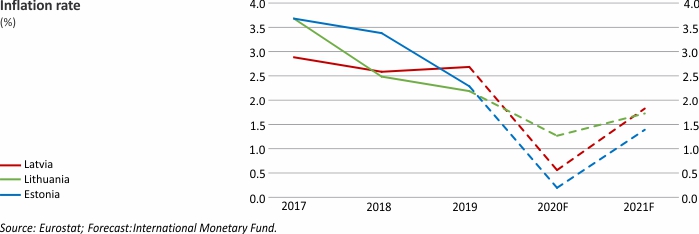

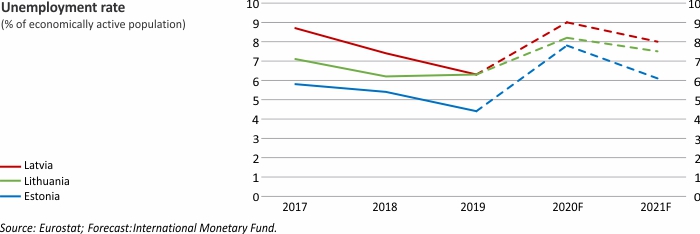

With businesses facing weaker demand, a rise in unemployment was observed in the labour market. Nonetheless, unemployment growth was markedly suppressed owing to the government support provided in the form of downtime benefits and on account of the tight labour market conditions that had existed before the crisis. In view of the above, the unemployment rate is projected to be approximately 8% in the near term. Furthermore, with the economy recovering, the unemployment rate is expected to decrease, inter alia, supported by relatively high labour market flexibility in Latvia. With the employment rate and hours worked decreasing, in the second quarter of 2020 the aggregate wage bill declined only slightly in annual terms. Meanwhile, the average wages in the economy continued rising. The labour market conditions are expected to be more favourable than projected before. Thus, while deflation will be observed in some months this year due to a decline in oil prices and a fall in the prices of individual services heavily affected by the pandemic, the inflation forecast has been revised upwards to 0.2% for 2020 and to 1.4% for 2021, bringing the inflation forecast closer to the 2% level in 2022.

Macroeconomic indicators – actual data and forecasts

Macroeconomic indicators – actual data and forecasts

Macroeconomic indicators – actual data and forecasts

Textual error

«… …»