Latvia's Macro Profile. June 2022

Latvijas Banka has published its latest June 2022 macroeconomic forecasts for Latvia. They have been drawn up in an environment of high uncertainty resulting from the unpredictable course of the war started by Russia and the related global price development.

Basic issues in brief:

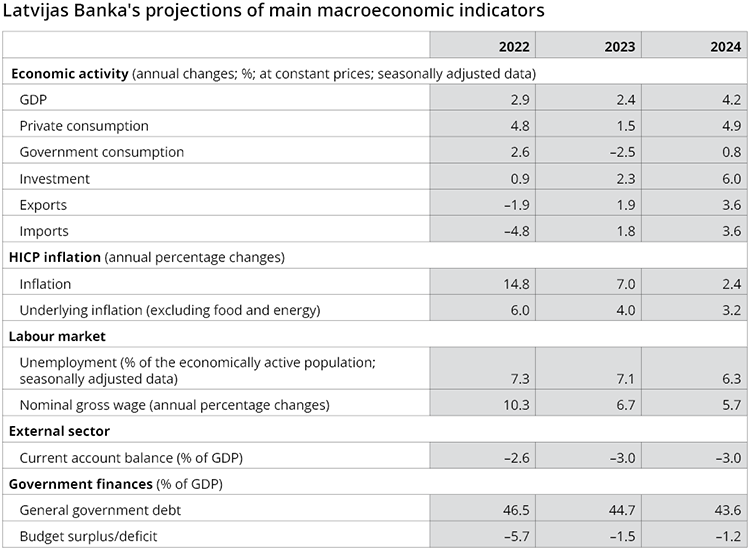

- The prolonged warfare has adverse effects on the outlook for economic growth in Latvia. However, the first quarter witnessed an unexpectedly good performance of the gross domestic product (GDP), allowing for an upward revision of the growth forecast for 2022 to 2.9% (March forecast was 1.8%).

- The rising prices and costs will weigh on economic activity at the end of the year. Therefore, the GDP growth forecast for 2023 has been revised downwards to 2.4% (March forecast was 3.2%).

- In 2024, the expected improvement in confidence allows for forecasting recovery of the pace of economic growth to 4.2% (March forecast was similar – 4.1%).

- The unfavourable development of the warfare impedes the availability of global resources and sustains input prices at a higher level for a longer period. This justifies an upward revision of the inflation forecast for 2022 and 2023 to 14.8% and 7.0% respectively (March forecast was 9.5% and 3.7% respectively).

- Inflation will decline to 2.4% in 2024 (March forecast was 2.1%) on account of the expected fall in energy futures prices driven by the anticipated improvement of the geopolitical situation.

Detailed analysis

Russia's invasion of Ukraine has significantly changed the economic environment, and the evolution of the warfare reinforces the current Covid-19 related disruptions in global supply chains, pressure from global energy, material and component prices, as well as uncertainty.

In the light of the new circumstances, the euro area inflation forecasts have been revised upwards significantly in June, whereas growth rates have been reduced for this year and next year.

The rise in inflation has changed the direction of monetary policy in most of the world's regions. It has been decided to reduce the monetary policy support and to raise interest rates, thus pushing up borrowing costs of the government and the private sector.

The inflation rate continues on an upward path in the euro area, and its pressure has broadened and strengthened, with prices of many goods and services surging. Against this background and in line with the previous forward guidance, the Governing Council of the European Central Bank (ECB) has taken decisions on the normalisation of the euro area accommodative monetary policy. In its June meeting, the ECB’s Governing Council decided to end net asset purchases as of 1 July 2022.

Moreover, the ECB’s Governing Council intends to raise the key ECB interest rates by 25 basis points at its July monetary policy meeting, starting the cycle of interest rate increase. It is expected that the key ECB interest rates will be raised again in September. The calibration of this rate increase will depend on the updated medium-term inflation outlook. It is also anticipated that gradual further increases in interest rates will be appropriate beyond September.

The rising global energy and food prices, as well as the increasing production costs also require an upward revision of the inflation forecasts for this year and the next one.

- Food and energy account for a large share in the consumption basket of Latvian households, and their prices are particularly surging. This makes inflation rise at a faster pace in Latvia compared to the countries having a smaller share of food and energy in their spending.

- The government support that allowed households to cover their expenses in the short term and reduce the contribution from energy prices to inflation has ended to a large extent.

- The wage growth, which is still maintained by labour shortages, coupled with higher material prices drive up production costs, and businesses try to transfer them to prices of their products.

The prolonged warfare worsens Latvijas Banka's perception regarding the outlook for economic growth in the second half of 2022.

- The strong growth observed in the first quarter of 2022 underpins GDP growth in the year as a whole. However, in the course of the year, towards the end of the year in particular, economic activity in Latvia might slow down significantly on account of the uncertainty stemming from the Russia-Ukraine war and the increases in costs and prices.

- The substantial relaxation of Covid-19 restrictions in March 2022 contributed to a strong recovery of the services sector.

- Inflation reduced the purchasing power of employees; however, consumption has increased at a rapid pace driven by the utilisation of the savings made during the pandemic.

- Economic ties with Russia and Belarus have been cut more gradually than was previously foreseen; moreover, replacement in export and resource markets has advanced quite smoothly.

- Some companies encounter difficulties due to business interruption with the aggressor countries. However, the economy as a whole witnesses a further decline in the number of the unemployed in the context of a shortage of labour.

- Consumption has been supported by the measures implemented by the government to address the energy and refugee crises.

Latvijas Banka's outlook on economic developments in the second half of 2022 has deteriorated.

- The skyrocketing energy and food prices will restrict people's purchasing power more radically and make their spending more cautious.

- The government support will continue to be relevant, and a targeted support would best reach vulnerable people, as well as would not contribute to fuelling the high inflation.

- Uncertainty and increasing costs will hamper the activity of private investment.

- The implementation of public investment projects by revising contracts whose costs have mounted due to the geopolitical situation acts as an important buffer for the economy.

- The outlook for exports is deteriorating owing to the weakening foreign demand and sustainability of competitiveness seen outside European markets.

- Amidst weakening demand, businesses may incline to revise their costs by reducing the number of employees, thus increasing unemployment.

The foreseen slowdown in economic growth at the year-end deteriorates the GDP growth projection for 2023. The improvement in consumer and business confidence expected in the event that the geopolitical situation stabilises in the region will contribute to growth recovery in the course of the next year and its continuation in 2024.

The fiscal support provided during the crises of energy prices and refugees in 2022 adds to budgetary expenditure. At the same time, the rise in public investment expenditure is relevant, in particular concerning security of energy supply and sustainability solutions. Risks of higher deficit relate to both promises made by parties before the Saeima elections and to the extension of flexibility of the European Commission's fiscal rules until 2024.

The cut-off date for the information used in the forecast is 24 May 2022, and 17 May for the information used in some technical assumptions.

Information about the latest forecasts is available in the macroeconomic forecasts section of Latvijas Banka's website macroeconomics.lv.

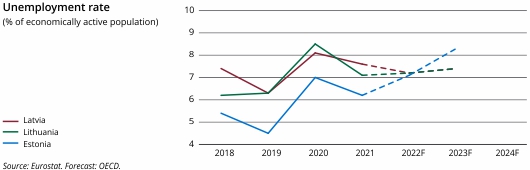

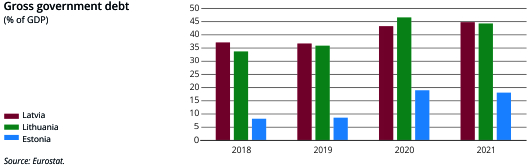

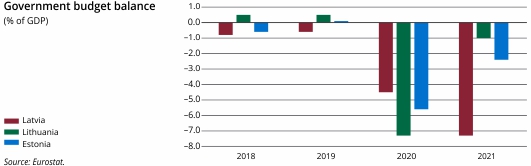

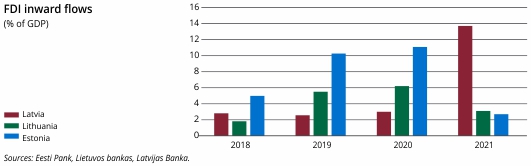

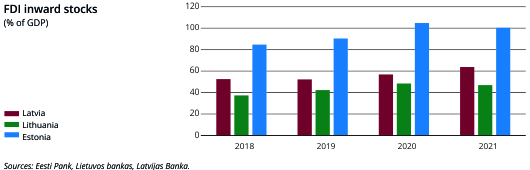

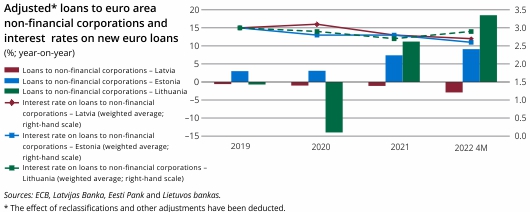

Macroeconomic Indicators: Latvia, Lithuania and Estonia

Textual error

«… …»