Going with the flow

The threat of the next flare-up of the pandemic has again shifted the prospects of returning to normal everyday life even further into the future, also with respect to deposits and lending. The persisting economic restrictions in Latvia and the upsurge in Covid infections in many countries in Europe and elsewhere in the world makes us find new ways to adapt to the current situation both by resuming or expanding consumption and increasing imports. The increase in spending has gradually dampened the surge in deposits observed during the first waves of the pandemic. Despite the changing sentiment, lending to households is becoming more active; however, the corporate loan portfolio still remains in the negative territory in annual terms, reducing the investment potential and thereby dampening the economic growth.

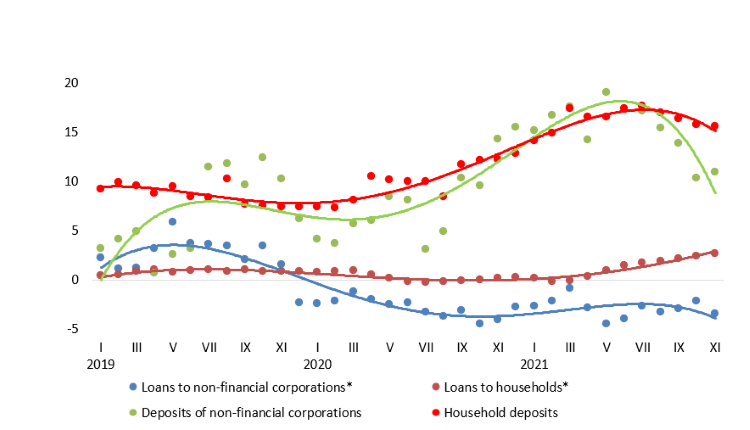

Domestic deposit growth has been rather moderate over the last three months, and their annual rate of increase dropped to 12.2% in November, down from 16%–18% reached in summer (inter alia, household and non-financial corporation deposits decreased to 15.6% and 10.9% year-on-year respectively). Household deposits grew in September, October and also in November, while those of non-financial corporations posted an increase only in November, following a two month decrease.

In September–November, the domestic loan portfolio saw relatively accelerated growth of 2%, albeit largely on account of one-off factors: in September, a branch of the Swedish TF Bank AB was opened in Latvia (up to now, the bank provided cross-border consumer lending services from Sweden; now the bank's consumer credit portfolio is reported in the total amount of domestic loans), whereas in October the leasing subsidiary OP Finance with its leasing portfolio was incorporated in the Latvian Branch of OP Corporate Bank. Along with persistently stable lending for house purchase, the annual growth rate of domestic loans (excluding government) reached 9.6% in November. Nevertheless, excluding the impact of the restructuring of the banking sector and the reclassification of institutional sectors, as well as that of one-off factors, the annual rate of change in the loan portfolio was a mere 0.7%, with the respective rates of loans to non-financial corporations and household loans standing at –3.5% and 2.6% respectively. In the third quarter of 2021, the domestic loan-to-GDP ratio remained unchanged at the low level of 39%, with lending to the real economy still remaining limited. Changes in new loans also confirmed the credit portfolio dynamics: in September–November, new loans to households increased by 10.2% in comparison with the previous three months, whereas new loans to non-financial corporations shrank by 8.2% over the same time period.

The potential rise in the number of Covid infections in Latvia due to the spread of omicron, the new Covid-19 variant, makes us remain highly cautious, therefore even spending during the holiday season is unlikely to cardinally reduce savings on bank accounts. As a result, a substantial shift in the current trends in deposits is highly unlikely at this stage. Meanwhile, more active corporate lending is one of the challenges for the next business cycle; the prolonged pandemic, however, persistently dampens the hopes for a more accelerated lending recovery. Let us hope that the public commitment to channel 4.5 billion euro to lending in 2022, announced by the major commercial banks in Latvia in December, will come true.

Annual changes in domestic loans and deposits (%)

* For the sake of comparability, the one-off effects related to the restructuring of Latvia's banking sector and the reclassification of the institutional sectors have been excluded.

Textual error

«… …»