The dynamics of productivity and wages is more balanced than in the pre-crisis period

For Latvijas Banka Monthly Newsletter, In Focus, September, 2018

Economists have been concerned about the overall dynamics of Latvia's economic productivity and wage increases for quite some time, trying to figure out whether the time has come to ring alarm bells regarding unbalanced development as productivity growth starts to lag behind. To understand whether these concerns are well-founded, it is worth looking at the indicators for individual industries and their contribution to the overall economic development.

When looking at the contribution of industries to changes in productivity, we see that manufacturing and trade are the largest contributors to overall growth due to their high share in the economy and rapid productivity growth. The third strongest contribution to changes in productivity comes from public administration, health and education.

Meanwhile, four sectors have recorded a decline in productivity: ICT services, financial and insurance activities, real estate activities and arts, entertainment and other services.

The dynamics of labour productivity and the factors affecting it vary across industries. The crisis in 2008–2010, leading to a rapid downturn in domestic and external demand, posed challenges for almost all sectors and countries across a wide geographical area. However, after the crisis the industries exhibit very different development trends.

There are sectors undergoing structural changes or having faced external demand related problems: the narrowing of the segment of credit institutions servicing foreign customers in the financial sector and the shrinking freight transportation by rail and by sea due to Russia shifting its freight flows to its own ports. Some industries (e.g. the manufacture of food products) were more hit by the Russian sanctions and affected by changes in the Russian ruble exchange rate in 2014–2015. These processes did not allow to ensure a high degree of capacity utilisation and had an adverse effect on profitability and also productivity. In these cases, we have to think about the export market and product diversification which has already been largely carried out by enterprises of the sectors.

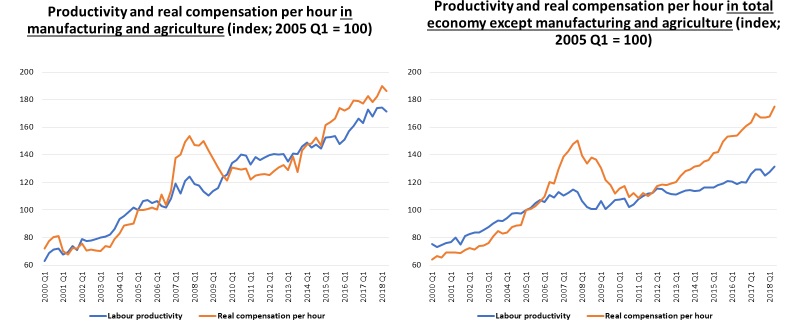

From the perspective of competitiveness, it is particularly important how wage and productivity indicators develop in the tradable or export-oriented industries; therefore, it is worth having an insight into the development of manufacturing and agriculture.

Labour productivity (real value added per hour worked) and compensation of employees per hour worked (real prices, 2005 = 100%)

The productivity of manufacturing and agriculture has been rising over the last two years along with wage developments; moreover, their productivity growth is much stronger than that of other industries. Thus, at this stage, the development of exporting sectors is relatively balanced, and the gap between wages and productivity mostly persists in the non-tradable segment.

Textual error

«… …»

Similar articles