Latvia's Macro Profile. June 2021

Latvia's Economic Developments and Outlook

Latvijas Banka has published its June 2021 macroeconomic forecasts, including the latest GDP and inflation forecasts, for Latvia.

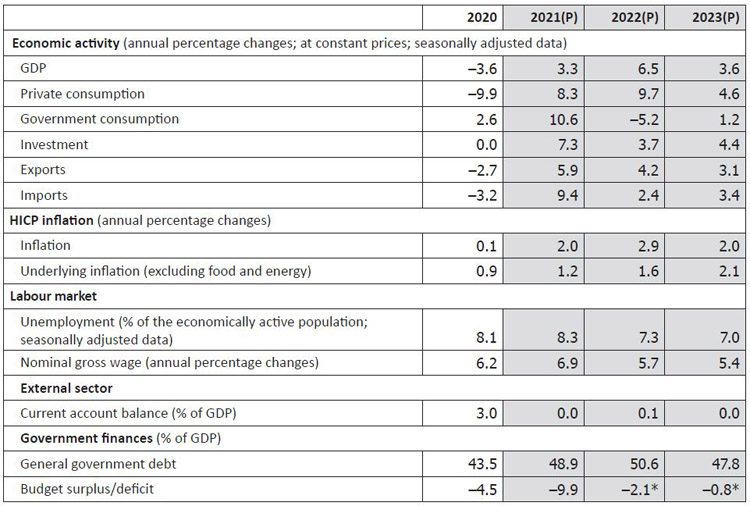

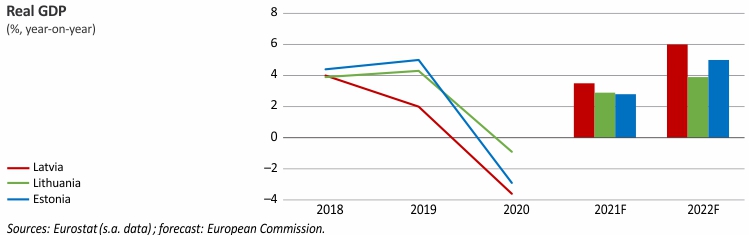

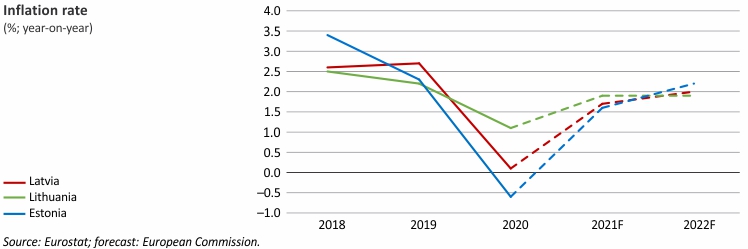

Latvia's GDP growth forecast for 2021 remains unchanged, with GDP projected to increase by 3.3% and 6.5% in 2021 and 2022 respectively. Meanwhile, Latvia's inflation forecast has been revised upwards to 2.0% in 2021 and to 2.9% in 2022, as compared to the March inflation forecast of 1.8% in 2021 and 2.2% in 2022.

With the number of vaccinated people growing and the Covid-19 infection rate declining both globally and in Latvia, the restrictions to contain the pandemic are being gradually eased. This, along with accommodative monetary policies implemented by major central banks and government support still provided to businesses and households, will ensure the global economic recovery. Such an upward trend in economic recovery was already included in Latvijas Banka's March forecasts; therefore, the June growth forecasts for 2021–2023 remain unchanged.

Meanwhile, inflation dynamics is affected by a rise in global demand causing a surge in commodity prices. On account of an increase in the global oil and food prices, Latvijas Banka has revised its inflation forecast upwards. While the underlying inflation will continue to increase, the factors associated with the rise in global commodity prices will stabilise, and in 2023 inflation is projected to stand at 2.0%, as compared to 1.8% projected in the March forecasts.

During the second wave of the pandemic in Latvia, the government continued and expanded its support as businesses and households adjusted to the pandemic conditions. Therefore, despite the restrictions enforced at the beginning of the year and the low mobility, in the first quarter GDP declined less than during the first wave of the pandemic.

The sentiment of economic agents and the employment expectations of businesses have improved rapidly since April. Retail trade and manufacturing sectors, too, are already posting good performance.

Further easing of restrictions will be reflected in economic growth as services will become more available and households will be able to spend their savings accumulated during the pandemic. These developments give reason to anticipate GDP growth of 3.3% already this year.

Along with high consumption, the funds available under the Recovery and Resilience Facility will increase over the coming years. Owing to resilient demand for the important export goods from Latvia, i.e. electronic products, wood as well as pharmaceutical and agricultural products, the record-high exports of the previous year will be exceeded. At the same time, risks remain with respect to supply chain disruptions as well as the sustainability of the strong demand for wood and high building material prices.

Looking at services exports, the sectors less dependent on face-to-face contacts continue to develop, while exports of travel and air transport services are expected to recover only after a more substantial improvement in the pandemic situation. With domestic demand stimulating import growth, the current account balance, after a significant surplus recorded last year, will again be close to zero.

Government support has helped businesses to meet their liquidity needs, prevented a wave of mass defaults and slowed down unemployment growth. With the economic situation improving, government support will become less intensive and there will be renewed need for targeted support to viable businesses as well as efficient insolvency proceedings, thus ensuring that resources are redirected to productive businesses.

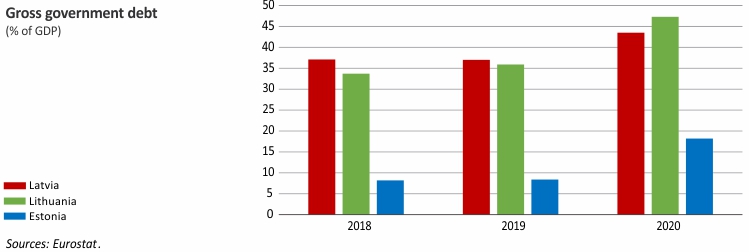

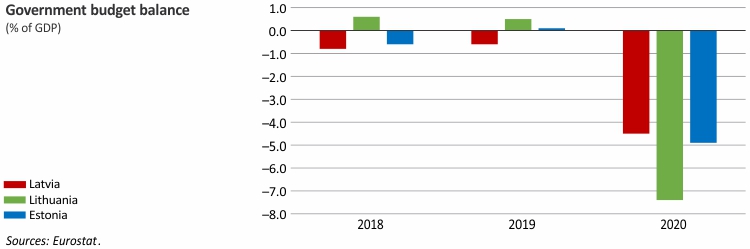

In view of the fact that the pandemic is retreating only gradually, the government support was extended for this year, and the social expenditure will increase in the following years, inter alia due to changes in the child-care benefit. Therefore, the general government budget deficit forecast for 2021 has been revised upwards to 9.9% of GDP. The budget deficit forecast for 2022 and 2023 stands at 2.1% and 0.8% of GDP respectively. The forecast is based on the no-policy-change assumption, only taking account of the currently adopted government decisions.

Given that, also in 2022, the European Union countries will be allowed for some flexibility established during the crisis with regard to the fiscal rules, the risks of a higher government budget deficit due to new policy initiatives are high. At the same time, it is important that the financial resources, available to Latvia under the European recovery plan, are invested to strengthen the foundations of the future economy.

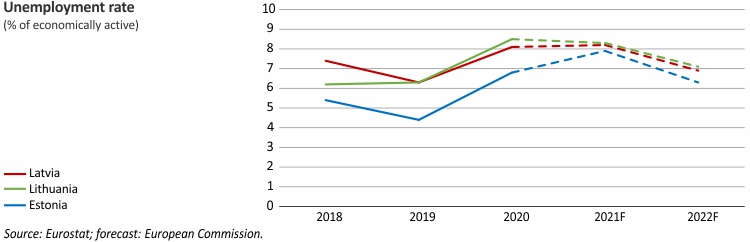

The rapid rise in wages and shrinking unemployment in the labour market contrasted with the decline in economic activity at the beginning of the year. At the same time, there was no improvement in employment opportunities. Nevertheless, the employment expectations of businesses improved, and the number of registered vacancies increased already in April. Yet, no rapid decline in unemployment is expected as the furloughed employees would be first to resume their work. Moreover, the hardest-hit sectors, which are also the most labour-intensive ones, are expected to recover only gradually. Latvijas Banka has not changed its estimate of a decline in the unemployment rate from 8.3% in 2021 to 7.0% in 2023.

A steep rise in wages was already projected in the first quarter. This was significantly influenced by the previously announced decisions on raising the minimum wage as well as the wages of medical and teaching staff. The availability of labour and the financial weakening of businesses operating in the sectors affected by the crisis could hold back wage increases. However, the shortage of labour already experienced before the crisis re-emerged in spring and the imbalance of skills became more apparent. This will sustain a rise in the average wage by 6.9% in 2021 and by almost 5.5% in the coming years.

As expected, the year-on-year consumer price inflation has turned positive since March, and it reached 2.6% in May. The rise in consumer prices is primarily driven by higher commodity prices in the global market and by higher service prices due to the pent-up demand and elevated costs caused by the social distancing measures, as well as by the significant increase in the minimum wage. According to Latvijas Banka's projections, inflation will stand at 2.0% in 2021. It will continue to move up and will reach its maximum level, i.e. above 3.5%, at the turn of 2021 and 2022. However, the rise in inflation should not be viewed as sustainable. While the underlying inflation is expected to grow further, the impact of the supply-side factors, i.e. the pressure of supply chain disruptions on commodity prices and the steep rise in oil prices during the recovery phase, is expected to subside, and inflation will stabilise at approximately 2%.

Macroeconomic fundamentals: actual data and Latvijas Banka projections (P)

The cut-off date for the information used in the forecast is 26 May 2021, and 18 May for the information used in some technical assumptions.

Textual error

«… …»